-This question was submitted by a user and answered by a volunteer of our choice.

Meaning of a Deferred Revenue

Deferred revenue is an amount received by an entity in advance before delivering the goods or transferring the title to goods or before rendering the services.

The concept of deferred revenue applies only if an entity follows the Accrual System of Accounting. If the entity follows the cash system of accounting it’s of no relevance as the entire amount received becomes income in the year of receipt.

Whether the Deferred Revenue is a Liability?

The answer to this question is “Yes” it is a liability. Even though you got the answer that it is a liability but I believe a part of the question remains unanswered i.e why is it a liability?

The logic for the same is: Since the entity has already received the amount even before rendering services or delivering goods the entity or a company has a sort of an obligation to deliver the goods or render such services at the predetermined future date. Failing which it may be liable to face legal proceedings or legal actions. Hence, it becomes a liability on a part of the entity to honour such a transaction.

When the entity receives the amount before delivering goods or rendering services that amount is recorded as a “Liability” and once the goods are delivered or services are rendered the liability is reduced and the entity records it as a “Revenue”.

For Example,

In the case of Educational Institutes like Universities, Coaching Institutes etc. it charges fees even before the term commences. In such a case the entity has not yet rendered service of imparting education hence, the tuition fees so received shall become a deferred revenue and shall be recorded as a liability at the time of the receipt and at as and when it’s accrued it shall be recorded as revenue.

Journal Entry for the same shall be;

At the time of receipt of Tuition Fees-

| Cash A/c | Debit | Debit the Increase in an Asset. |

| Deferred Revenue A/c | Credit | Credit the Increase in a Liability. |

And at the time of recording revenue on monthly basis every month;

| Deferred Revenue A/c | Debit | Debit the Decrease in a Liability. |

| Tuition Fees Earned A/c | Credit | Credit the Increase in an Income. |

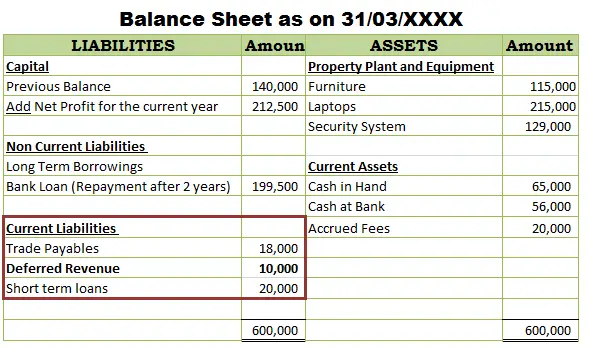

Deferred Revenue is Presented in the Balance Sheet as;

Conclusion

Deferred revenue at the time of early receipt of the amount is recorded as a liability and at the time of actual income recorded as revenue in the income statement.