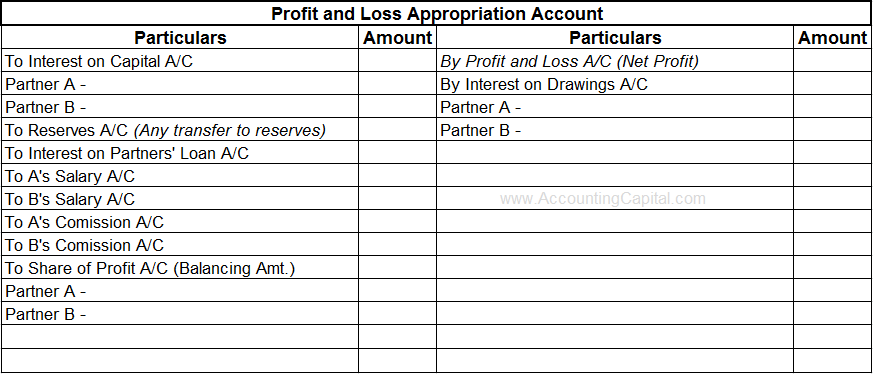

Profit and Loss Appropriation Account

In case of a sole proprietorship, there is a single owner and any addition in the capital in form of net profit or reduction in form of drawings is directly done from the firm’s capital account. However, in case of a partnership, “Profit and Loss Appropriation Account” is created to demonstrate the change in each partner’s individual capital as a result of profit or loss incurred by the firm.

P&L Appropriation account helps to show a clear distinction between the capital contribution of each partner and the changes thereafter. Profit and Loss Appropriation Account is used for allocation of net profit among different partners. It is seen as an extension of the profit and loss account itself.

Template and Method of Preparation

It includes items such as interest on capital, interest on drawings, interest on partner’s loan, salaries to partners, commission, reserves, and profit share. (It doesn’t include drawings made by partners)

Credit

Net Profit (From the income statement) & Interest on drawings (charged to partners)

Debit

Interest on capital, salaries to partners, commission to partners, transfer to reserve, profit share, etc.

Note – Except rent if there are any funds payable to a partner for e.g. interest on capital, salaries, commission, etc. they should be treated as appropriation and are not supposed to be charged against profits.

Short Quiz for Self-Evaluation

>Read Difference Between Profit and Loss & Profit and Loss Appropriation