Journal vs Ledger

During the accounting cycle, there are two important steps to be followed; recording journal entries & preparing ledger accounts. They are related, however, there is a difference between journal and ledger which can be summarized as follows;

Journal

1. Journal is a book of accounting where daily records of business transactions are first recorded in a chronological order i.e. in the order of dates.

2. It is known as the primary book of accounting or the book of original/first entry.

3. It is prepared out of transaction proofs such as vouchers, receipts, bills, etc.

4. A journal is not balanced like a ledger.

5. The procedure of recording in a journal is known as journalizing, which performed in the form of a Journal Entry.

6. It may be subdivided into a cash book, a sales day book, sales return day book, purchases day book, purchases return day book, B/R Book, B/P Book, Petty Cash Book.

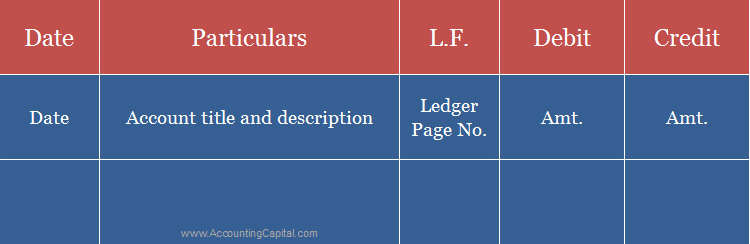

7. The format of a journal;

Related Topic – What is a Compound Journal Entry?

Ledger

1. A ledger is an accounting book in which all similar transactions related to a particular person or thing are maintained in a summarized form.

2. It is known as the principal book of accounting or the book of final entry.

3. It is prepared with the help of a journal itself, therefore, it is the immediate step after recording a journal.

4. Except for nominal accounts, all ledger accounts are balanced to find the net result.

5. The procedure of recording in a ledger is known as posting.

6. It may be sub-divided into general ledger, debtors/sales ledger, creditors/purchases ledger.

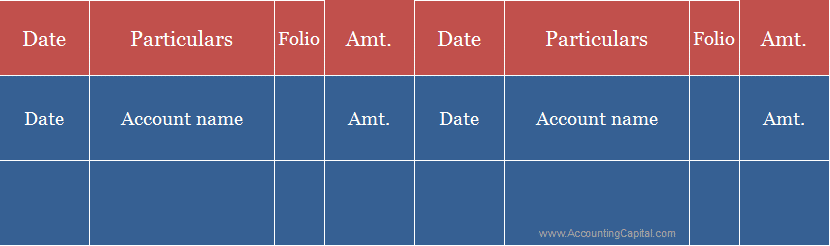

7. The format of a ledger account;

>Read How to Make a Trial Balance from Ledger Balances?