Bad Debts

In a business scenario, amounts which are overdue to a business owner by the debtor(s) and declared irrecoverable are called bad debts. Few reasons for debtors to not pay their debts on time may be; filing for bankruptcy, experiencing hardship due to losses, etc.

This can either be the complete amount owed or a part of the debt. Sometimes the amount may be recovered (partially or fully) in future. This is recorded with a journal entry for the recovery of debts.

While accounting for b/debts it is treated as a loss to business and reduces the total accounts receivable. The full amount should be written off to the “Income statement” of the related period or against the provision for doubtful debts. They are losses, hence they are debited and the debtor’s account is credited.

Journal Entry for Bad Debts

| Bad Debts A/C | Debit | Nominal Account | Dr. all losses |

| To Debtor’s A/C | Credit | Personal Account | Cr. the giver |

As per modern rules of accounting;

| Bad Debts A/C | Debit | Loss | Dr. the increase in loss |

| To Debtor’s A/C | Credit | Asset | Cr. decrease in asset |

At the time of preparing final accounts, debts which are written off during the period post-finalization of trial balance are transferred to the profit and loss account by recording the below journal entry.

| Profit & Loss A/C | Debit |

| To Bad Debts A/C | Credit |

Related Topic – Difference Between Discount and Rebate

Explanation with Example

Let us assume that Mr Unreal, a sole proprietor, was supposed to pay 1,00,000 on an invoice to ABC Corp. However, he filed for bankruptcy and is declared insolvent. In this case, ABC Corp will go through the following accounting in their books:

At the time of realization (Assuming the opening balance was nil)

| Bad Debts A/C | 1,00,000 |

| To Mr Unreal A/C | 1,00,000 |

At the time of transferring the amount to the P&L Account

| Profit & Loss A/C | 1,00,000 |

| To Bad Debts A/C | 1,00,000 |

Related Topic – What are Non-performing assets or NPA?

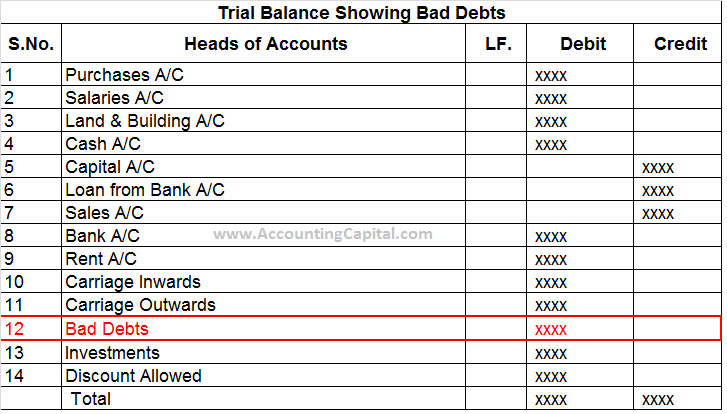

Bad Debts Shown in Trial Balance

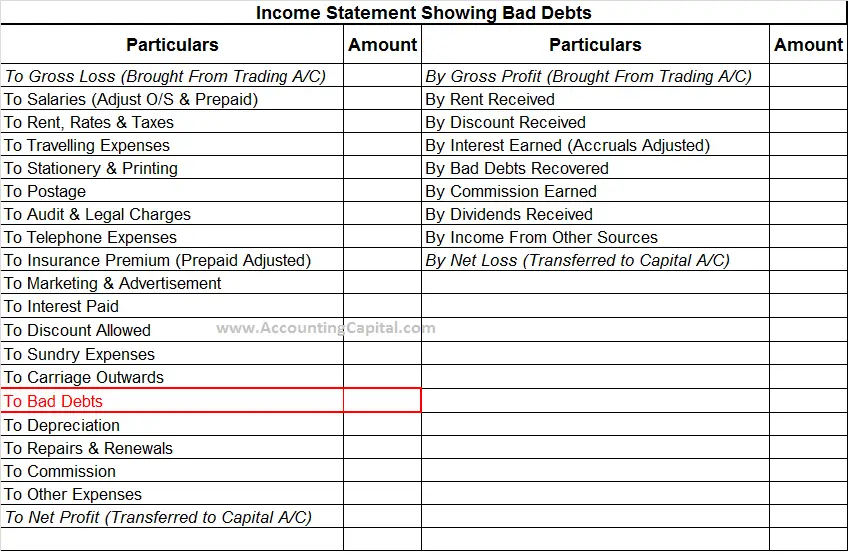

Bad Debts Shown in Income Statement

Short Quiz for Self-Evaluation

>Read Provision for Discount on Debtors