Balance B/F and Balance C/F

In bookkeeping, Balance B/F and Balance C/F are a couple of accounting jargon used while journalizing. They play a role in totalling and carrying forward balances from one page of the journal book to the next one.

Balance B/F – Balance Brought Forward | Balance C/F – Balance Carried Forward

To understand balance b/f and balance c/f begin with understanding carried forward first and brought forward next.

Example – Balance C/F

The journal book maintained by a business includes many journal entries, due to a large number of entries multiple pages of the journal book are used.

At the end of a journal page, debit and credit balances are totalled and carried forward to the next page, this balance pushed forward from the current page to the next page is termed as “Balance C/F” or “Total C/F” (Carried Forward).

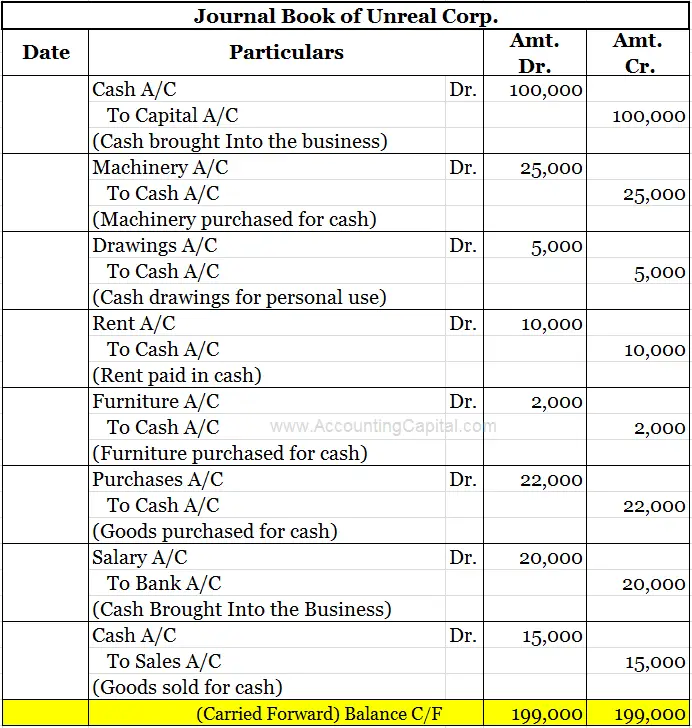

Below is a sample journal book for Unreal Corp.

Highlighted in yellow is the total of both debit and credit sides on this page of the journal book, this balance will be carried forward to the next page & should be treated as the opening balance of the next page.

Related Topic – What is Bookkeeping?

Example – Balance B\F

At the beginning of a new journal page, the opening balance is quoted from the previous page, this balance pulled forward from the previous page to the current page is termed as “Balance B/F” or “Total B/F” (Brought Forward).

Consequently from the above example when Unreal Corp. moves to the next page of its journal book it will bring both the closing debit and credit balance from the previous page.

Below is a sample of the journal book for Unreal Corp. (Next Page)

Balance B/F & Balance C/F are used in journal books whereas Balance B/D & Balance C/D are used with ledger accounts.

Short Quiz for Self-Evaluation

>Read Balance B/D and Balance C/D