-This question was submitted by a user and answered by a volunteer of our choice.

Yes, the cash book is both a journal and a ledger.

To make the concept simpler, let us first be familiarized with the meaning of journals and ledgers, which shall help in determining the reasons for a cashbook to be both a journal as well as a ledger.

What is a Cashbook?

A Cashbook is a book of original entries that records all the cash and bank transactions. It may be a single-column, double-column, or triple-column cash book.

- Single-column Cash Book: In a single-column cash book, there is only one column and it records the cash transactions.

- Double-column Cash Book: In a double-column cash book there is one column each for cash and bank transactions.

- Triple-column Cash Book: In a triple-column cash book there are three columns, one each for cash transactions, bank transactions, and discounts allowed and received.

What is a Journal?

A Journal is a descriptive financial record of a business that is used for future reconciling as well as a transfer to other books of accounts such as the ledger. It is a book of original entries.

Cashbook is considered to be a journal because all the cash/bank receipts and payments are recorded in this book in a descriptive form similar to journal posting.

What is a Ledger?

In simple words, a ledger refers to recording individual accounts in a summarized form that are posted from a journal. It is a book of principal entries.

A cashbook is considered to be a ledger because all the cash transactions that are made during a particular financial period are recorded in this book in chronological order.

When a cashbook is prepared there is no need for a cash a/c as the book serves the same purpose and therefore, it can be used as a substitute.

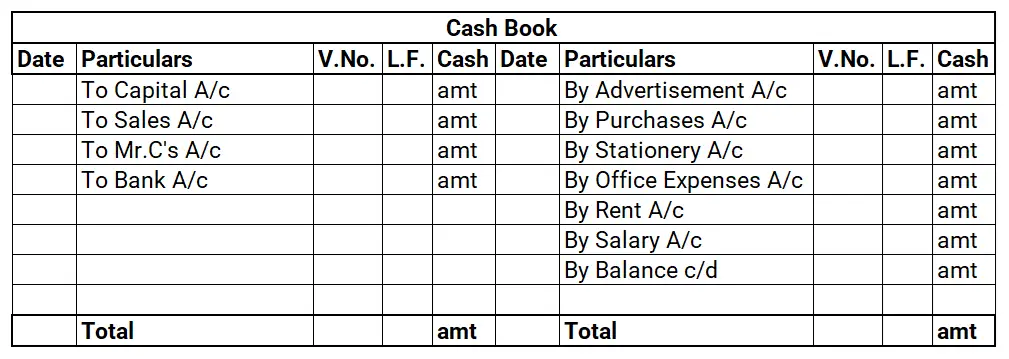

What is the Format of a Cashbook?

The format of a Cash book is given in the image below:

Note: We may observe from the above image that the format and posting of a cashbook are similar to that of journal and ledger accounts. Therefore, it is right to say that a Cash book is both a Journal and a Ledger.

Conclusion

The above article may be summarised as follows:

- A Cashbook is a book of original entries that records all the cash and bank transactions.

- It is both a Ledger and a Journal.

- It may be a single-column, double-column, or triple-column cash book.

- It is a book of original entries, hence, it is considered a Journal.

- All the transactions of a year are recorded in the cash book and therefore, it is also a ledger.