-This question was submitted by a user and answered by a volunteer of our choice.

Objectives of Bank Reconciliation Statement

Bank Reconciliation statement refers to the statement that reconciles the difference between the balances as per the bank column of cash-book and pass-book. The following are the objectives of the bank reconciliation statement. BRS Stands for Bank Reconciliation Statement.

1. The primary objective for preparing BRS is to check the accuracy in the bank column of both cash book and passbook. Accountants generally prepare BRS based on transactions recorded in the cash book and bank book (passbook) at a particular time.

2. BRS is prepared to check the cash inflows and outflows in the business and they must tally with the bank statements (or) passbook. This helps the users to easily detect the non-uniformity in cash book balance and passbook balance.

3. BRS provides us information on the various aspects of banking transactions such as it gives information on the position of cheques, payment made by the bank on standing instructions, direct payment by debtors, bank charges, bank interest, dividends received etc.,

4. BRS helps the accountant to keep track of the funds available in the bank account. Hence it becomes comfortable for the company to issue a cheque for making payments to its various creditors in some future agreed date.

5. Another main objective of preparing BRS is to control the internal management of the organization on cash inflow and outflow. BRS acts as a mechanism to keep track of cash embezzlement, bank drafts and misuse of the company’s funds by dishonest employees.

Impact of Bank Reconciliation Statements

The following impact may occur if companies do not prepare bank reconciliation statements.

1. If the bank reconciliation statements are not prepared by the companies then there will be a difference in the bank column of cashbook and passbook. Hence, there will not be any accuracy in amounts of cashbook and passbook.

2. If the bank reconciliation statement is not prepared then the company will not have adequate information relating to the various banking transactions such as payment made to various creditors, bank interest, bank charges, dividends received etc.,

3. If the bank reconciliation statement is not prepared then it will be very difficult for an accountant to keep track of available funds in the bank account as per the passbook. This may result in the delay of future payment to suppliers, creditors and other agents.

4. If the bank reconciliation statement is not prepared by the companies then cash embezzlement, fraudulent transactions, misuse of company funds by dishonest employees will increase and it cannot be easily traced by the company.

I would like to add an example for a clear understanding of the above explanation

Example for Bank Reconciliation Statement

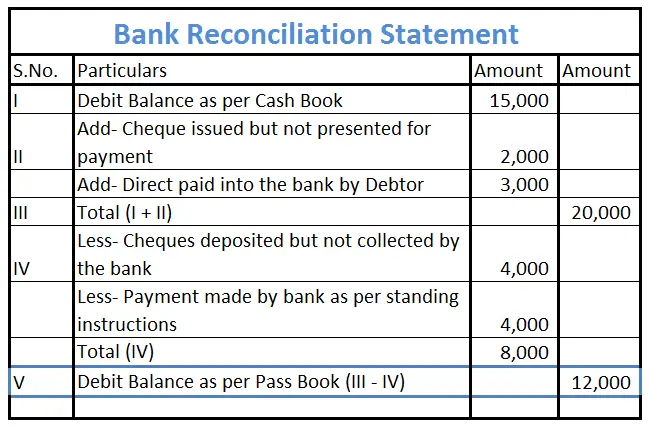

ABC Ltd furnishes you the following information prepare a Bank Reconciliation Statement to find out the Debit Balance of Pass Book.

| Sno | Particulars | Amount |

| I | Debit Balance as per Cash Book | 15,000 |

| 1. | Cheques issued but not presented | 2,000 |

| 2. | Cheques deposited but not collected | 4,000 |

| 3. | Payment made by the bank as per standing instructions | 4,000 |

| 4. | Direct deposit by customers in the bank | 3,000 |

Bank Reconciliation Statement of ABC Ltd.

Impact of Transaction if bank reconciliation statement not prepared

If the cheque is deposited but not collected,

CashBook– The accountant will record the transaction and it will show an increase in the bank balance of the cashbook (15,000+4,000 = 19,000).

PassBook– If the same is not recorded by the bank at the same time. Then the bank passbook will show the same balance (say- no increase and no decrease).