-This question was submitted by a user and answered by a volunteer of our choice.

Fixed Assets

Fixed assets are those assets that can be in the firm for a long period and it is tangible. These assets provide benefits for more than one accounting period for the firm. These provide support for the production or delivery of goods or services.

Current Assets

Current assets are those assets that are used within the operating year. These assets are used for the company’s day-to-day operations. This shows the firm’s liquidity and its ability to meet short-term obligations.

List of Fixed Assets and Current Assets

| Fixed Assets | Current Assets |

| 1. Plant & Machinery | 1. Cash |

| 2. Land | 2. Cash Equivalents |

| 3. Equipment | 3. Short-Term Deposits |

| 4. Furniture & Fixtures | 4. Inventory |

| 5. Vehicles | 5. Marketable Securities |

| 6. Leasehold Improvements | 6. Office Supplies |

| 7. Computer Software | 7. Trade Receivables |

| 8. Buildings | 8. Short Term Borrowings |

| 9. Patents | 9. Accounts Receivables |

| 10. Trademarks | 10. Prepaid Expenses |

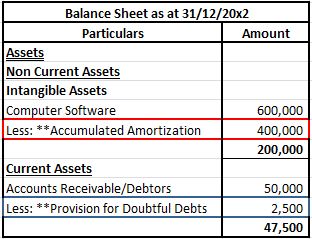

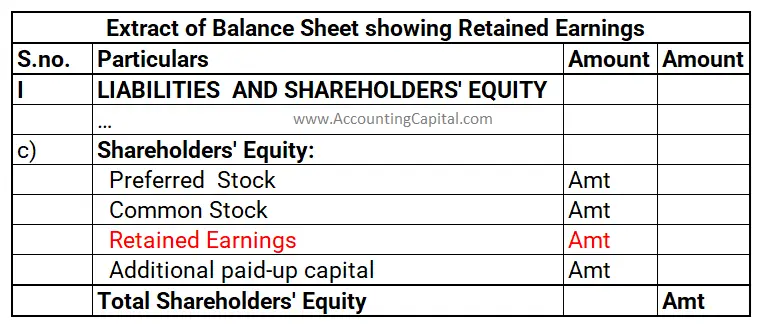

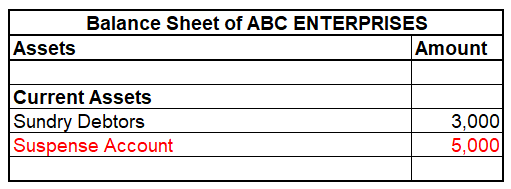

Presentation in the balance sheet

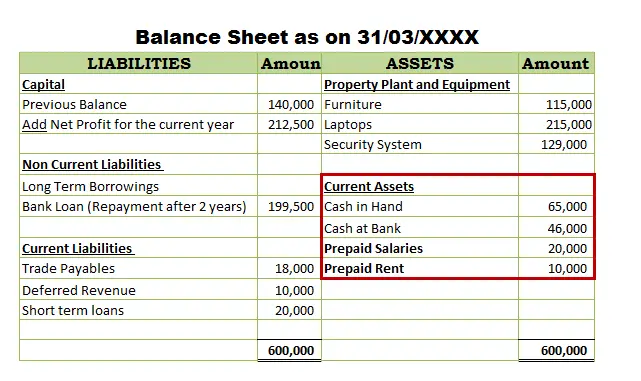

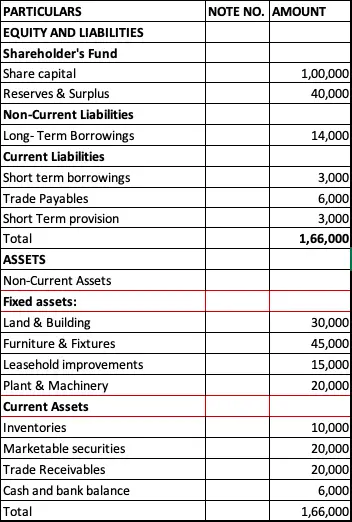

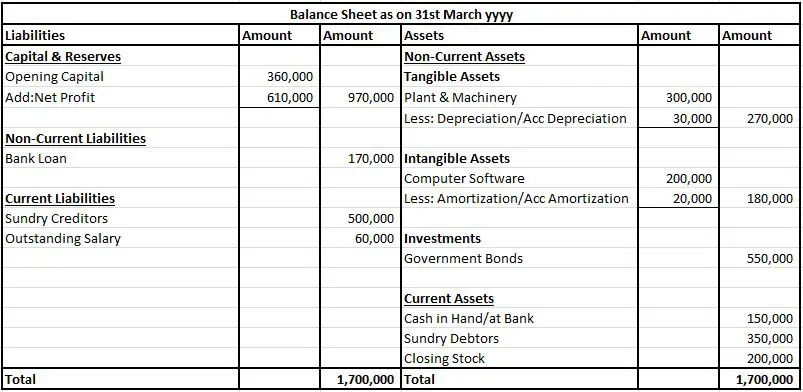

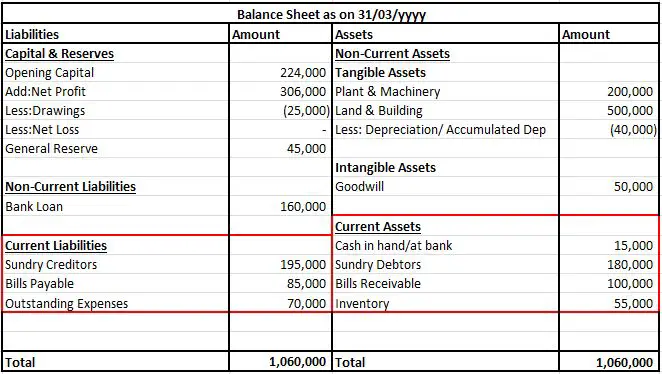

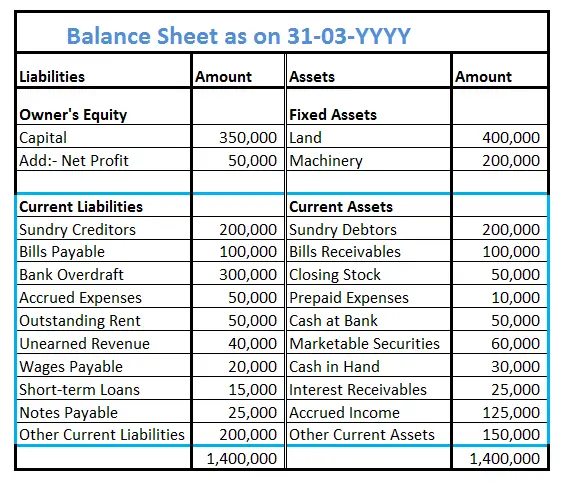

The balance sheet of ABC Ltd. is as follows;

This is an example of a balance sheet. The liabilities are recorded first and later assets are recorded. Assets and liabilities must balance out each other.

It is important to record all the liabilities as the company needs to pay them back responsibility on time. The assets also need to be recorded to know what kind of assets the company owns.

The fixed assets are recorded first since they stay for more than one accounting period. Later, the current assets are recorded since they will be used up within an operating year. All of the assets need to be mentioned in the company and should be organized based on the category it belongs to like fixed assets and current assets.

Conclusion

It is important and necessary for the company to be transparent about its assets and liabilities to the public.

>Related Long Quiz for Practice Quiz 20 – Current Assets

>Related Long Quiz for Practice Quiz 35 – Fixed Assets

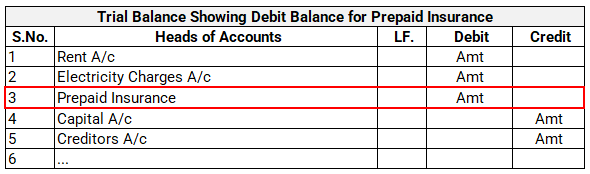

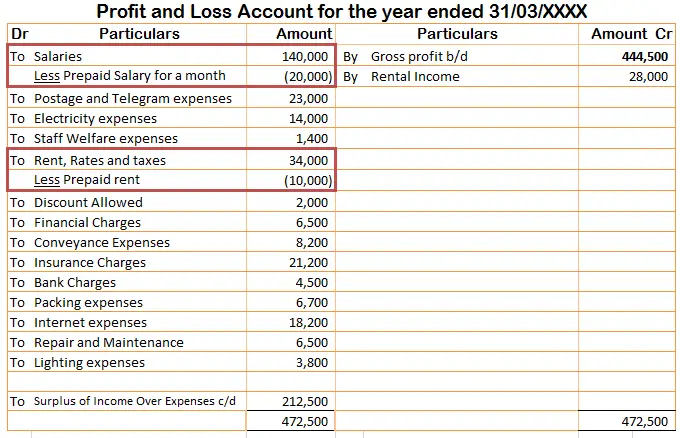

The prepaid expenses are reduced from the expenses in the profit and loss account as it is being utilized during the operating year and it slowly reduces the value of the current asset.

The prepaid expenses are reduced from the expenses in the profit and loss account as it is being utilized during the operating year and it slowly reduces the value of the current asset.