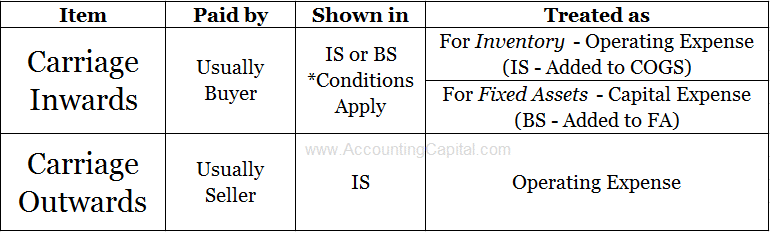

Carriage Inwards and Carriage Outwards

“Carriage” can be seen as freight or transportation cost, it is the carrying costs related to the purchase and sale of goods. Often the buyer is responsible for the cost of carriage inwards whereas the seller is responsible for carriage outwards. Carriage inwards and carriage outwards are essentially delivery expenses (revenue expenditure) related to buying and selling of goods.

Charges may be incurred while goods are purchased or when they are sold. Depending on the type of asset in question, carriage expense may or may not be capitalized. For example, in the case of carriage-paid to acquire a fixed asset, it is treated as a capital expenditure and added to the amount of the fixed asset.

When Goods are Brought In

It is the freight and shipping cost incurred by a business while purchasing a new product. The product may be for company use or for resale, the word “Inwards” shows that the cost is incurred while the goods are being brought into the business. Carriage inwards is also called freight-in and transportation-in.

Mostly the buyer is responsible for carriage inwards.

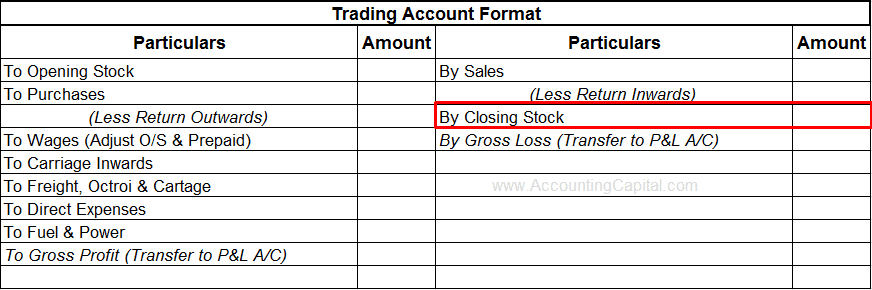

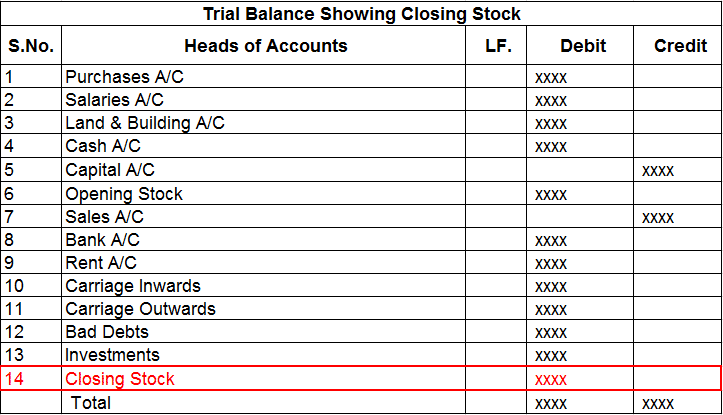

In case of procurement of fixed assets carriage inwards is capitalized which means the cost of carriage is added to the fixed asset. In case of purchasing inventory for resale, the amount is treated as a direct expense (added to COGS) and is shown on the debit side of a trading account.

Related Topic – Journal Entry for Carriage Inwards

When Goods are Sent Out

It is the freight and shipping cost incurred by a business while selling a product. The word “Outwards” shows that the cost is incurred while the goods are being sent out of the business. Carriage outwards is also called freight-out and transportation-out.

Mostly the seller is responsible for carriage outwards.

Carriage outwards is a revenue expense for the business and should be shown on the debit side of an income statement.

Short Quiz for Self-Evaluation

>Read Journal Entry for Carriage Outwards

Note – It is represented as a percentage so it is multiplied by 100.

Note – It is represented as a percentage so it is multiplied by 100.