Nowadays, businesses sell their assets as part of strategic decision-making. Reasons could vary from up-gradation to new better quality asset, arranging money for a business need, not in use asset etc. there could be any reason to sell an asset.

It is common that an asset may not be sold at its current book value if it is sold for more, it generates profit for the business and, in the situation opposite to that, it incurs a loss when it is sold for less.

Journal entry for loss on sale of fixed assets is shown on the debit side of profit and loss account.

There are 3 different accounts that will be affected by this

The asset being sold

The cash being received

A loss incurred on the sale of an asset

Journal Entry for Loss on Sale of Fixed Assets

Cash A/C

Debit

Real Account

Debit what comes in

Loss on sale of asset

Debit

Nominal Account

Debit all losses

To Sale of Asset

Credit

Real Account

Credit what goes out

Short Quiz for Self-Evaluation

Loading

Your quiz has been submitted

Want to re-attempt? - Simply “refresh” this page.

Please check out more content on our site :)

Subscribed? - Check your mailbox

Thank You!

Server Side Error

We faced problems while connecting to the server or receiving data from the server. Please wait for a few seconds and try again.

If the problem persists, then check your internet connectivity. If all other sites open fine, then please contact the administrator of this website with the following information.

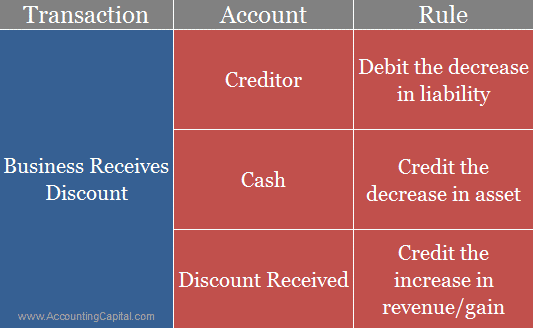

Discounts are common in both B2B and B2C transactions to push both credit and cash sales, they are usually given in lieu of some consideration which can be prompt payments, trade practices, recoveries, etc. While posting a journal entry for discount received “Discount Received Account” is credited.

Discount received acts as a gain for the business and is shown on the credit side of a profit and loss account. Trade discount is not shown in the main financial statements, however cash discount and other types of discounts are shown in books of accounts.

Journal entry for discount received is essentially booked with the help of a compound journal entry.

Discount received by a buyer is discount allowed in the books of the seller. Following examples explain the use of journal entry for discount received in the real-world scenarios.

Examples – Accounting for Discount Received

Payment made to Unreal Co. in cash for goods purchased worth 5,000 at 10% discount. (Discount received in the regular course of business)

Unreal Co. A/C

5,000

To Cash A/C

4,500

To Discount Received A/C

5,00

Paid 2,000 to Unreal Co. in cash for full and final settlement of their account worth 10,000. (Discount received to settle an overdue payment)

Unreal Co. A/C

10,000

To Cash A/C

2,000

To Discount Received

8,000

Short Quiz for Self-Evaluation

Loading

Your quiz has been submitted

Want to re-attempt? – “Refresh” this page.

Check out more content on our site :)

Subscribed? – Check your mailbox

Thank You!

Server Side Error

We faced problems while connecting to the server or receiving data from the server. Please wait for a few seconds and try again.

If the problem persists, then check your internet connectivity. If all other sites open fine, then please contact the administrator of this website with the following information.

Return outwards are goods returned by a customer to the seller. They are goods that were once purchased from external parties, however, because of being unsatisfactory they were returned back to them, they are also called Purchase returns.

Outward returns reduce the total accounts payable for a business. It is a sales return and on the other, it is a purchase return. The transaction in both cases is reversed and the related sale or purchase is nullified.

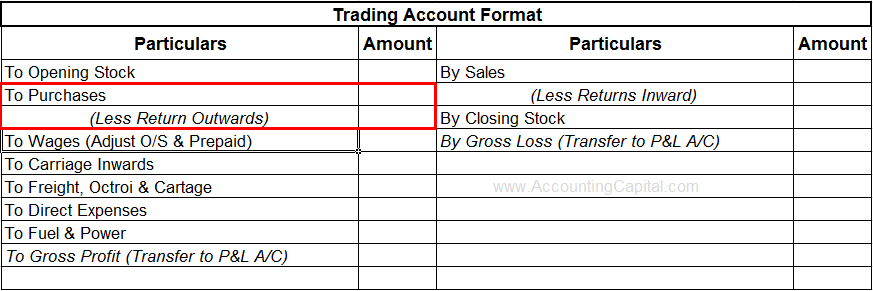

Purchase returns reduce the total purchases/accounts payable of a company and the deduction is shown in the trading account. A subsidiary book called Purchase returns book is prepared to record all such entries.

Journal Entry for Return Outwards

Supplier’s A/C

Debit

Debit the decrease in liability

To Return Outwards A/C

Credit

Credit the decrease in expense

Supplier – This is a reduction in payables for the business.

Return Outwards – This is a reduction in expenses for the business.

Shown in Trading Account (Deducted from Purchases)

Let’s suppose that a company “Unreal Pvt Ltd.” returned goods worth 10,000 to its supplier “Star Pvt Ltd.”. The journal entry to record these returns in the books of Unreal Pvt Ltd. will be as follows;

Star Pvt Ltd. A/C

10,000

To Return Outwards A/C

10,000

Reasons for Purchase Returns

An incorrect product or size was ordered by the customer. (customer’s mistake)

An incorrect product or size was sent by the seller. (seller’s mistake)

Damaged or defective products received. (product damaged)

The quality of the product was not as expected. (bad quality)

Late delivery of the product. (timing)

The buyer purchased an excessive amount. (quantity)

Better price found by the buyer with another seller. (price options)

Short Quiz for Self-Evaluation

Loading

Your quiz has been submitted

Want to re-attempt? - “Refresh” this page.

Check out more content on our site :)

Subscribed? - Check your mailbox

Thank You!

Server Side Error

We faced problems while connecting to the server or receiving data from the server. Please wait for a few seconds and try again.

If the problem persists, then check your internet connectivity. If all other sites open fine, then please contact the administrator of this website with the following information.

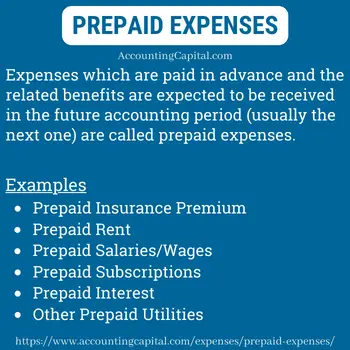

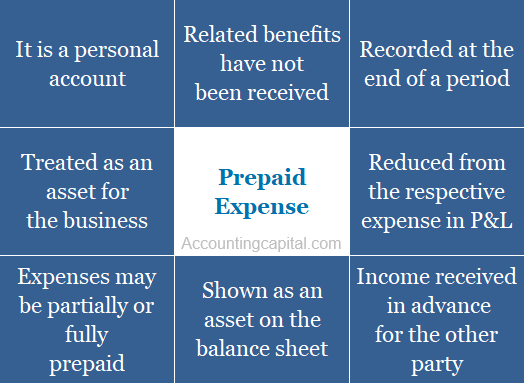

Prepaid expenses are those expenses which have been paid in advance and the related benefits are not received within the same accounting period. The benefits of expenses incurred are carried forward to the next accounting period. Prepaid expenses are treated as an asset by the business.

Examples – Prepaid salary, prepaid rent, prepaid subscription, etc. They are recorded in books of finance at the end of an accounting period to show the true numbers of a business. They are also known as unexpired expenses or expenses paid in advance.

Examples

Company-A has a rent obligation of 80,000/year that is due every time on the 10th of Jan, this year the company decides to pay double that is full rent in advance for next year.

The amount paid in advance for next year is 80,000 which is prepaid and termed as a “prepaid expense” for Company A.

At the end of the period, this “amount paid in advance” impacts the financials of the business. Such a transaction is supposed to be journalized.

According to the accrual concept of accounting, transactions are recorded in the books of accounts at the time of their occurrence and not when the actual cash or a cash equivalent is received or paid.

Based on the above principle, payments are not necessarily made immediately they may be late or in advance. Outstanding expenses and unexpired expenses are both a result of this.

Advance payment made for an expense has two steps for being recorded and recognised. Firstly, when the prepayment is done and secondly when the related expense becomes due.

a) At the time of advance payment of the expense.

Prepaid Expense A/c

Debit

Debit the increase in asset

To Bank A/c

Credit

Credit the decrease in asset

(Being expense paid in advance for the period)

b) At the time when the expense becomes due to be paid.

Expense A/c

Debit

Debit the increase in expense

To Prepaid Expense A/c

Credit

Credit the decrease in asset

(Adjustment entry made to recognize the expense on the due date)

Alternate Scenario

In some cases, expenses are prepaid along with the actual payment made on the due date. In such a case, when the date is the same then a compound journal entry can also be recorded.

Expense A/c

Debit

Debit the increase in expense

Prepaid Expense A/c

Debit

Debit the increase in asset

To Bank A/c

Credit

Credit the decrease in asset

(Being expense paid along with prepaid expense paid in advance for a future period)

Prepaid Expenses in Trial Balance

If prepaid expense already appears inside the trial balance then it implies that the adjusting entry has already been posted.

In this case, it is only shown on the balance sheet as a “current asset” and no adjustment is required in the income statement.

In the event that such an expense does not appear in the trial balance, they should be added to the respective accounts. This should be reflected on the debit side of the Profit and Loss Account.

An insurance premium is an amount paid to cover the cost of coverage associated with an insurance agreement. It is often paid monthly, quarterly, half-yearly, or yearly.

When an insurance premium has been paid to the insurance company but the related coverage hasn’t yet begun, this is known as insurance premium prepaid.

Prepaid insurance journal entry should be recorded as follows:

a) At the time insurance premium is prepaid.

Prepaid Insurance Premium A/c

Debit

To Bank A/c

Credit

(Being insurance premium paid in advance)

b) On the date the prepaid insurance premium becomes due.

Insurance Expense A/c

Debit

To Prepaid Insurance Premium A/c

Credit

(Insurance expense being recognized and the related prepaid asset being reduced)

When the insurance premium is due, the amount due is deducted from the prepaid account and is shown as an operating expense in the Profit and Loss A/c prepared for the current period.

The term “rent” refers to a periodic payment that covers the expenses associated with occupying and using a property (such as land, buildings, etc.) The payments are made to the owner of the property. Usually, it is paid on a monthly or annual basis.

The term “outstanding rent” refers to rent due for a period that has already passed.

Prepaid rent journal entry should be recorded as follows:

a) At the time rent is paid in advance.

Prepaid Rent A/c

Debit

To Bank A/c

Credit

(Being rent paid in advance)

b) On the date the prepaid rent becomes due.

Rent Expense A/c

Debit

To Prepaid Rent A/c

Credit

(Rent expense being recognised and the related prepaid asset being reduced)

On the date when rent expense is actually due, the amount is deducted from the prepaid rent account and is shown as an operating expense in the Profit and Loss A/c prepared for the current period.

In exchange for the work that an employee performs, an employer pays them a salary. It is often paid monthly and accompanied by some benefits.

When a salary is paid in advance to an employee but the employee is yet to work for that period it is called salary paid in advance.

Prepaid salary journal entry should be recorded as follows:

a) At the time salary is prepaid.

Prepaid Salaries A/c

Debit

To Bank A/c

Credit

(Being salary paid in advance)

b) On the date the salary becomes due.

Salaries A/c

Debit

To Prepaid Salaries A/c

Credit

(Salary expense being recognized and the related asset being reduced)

When the actual salary is due, the amount is deducted from the prepaid salaries account and is shown as an operating expense in the current period’s Income Statement.

Assets are resources that belong to a person or entity. They may be tangible or intangible items used to generate economic value for business operations. An expense that is paid before it is due is considered prepaid and it is treated as an asset (current) for the business.

Reason – The logic of why advance payment made for an expense is treated as an asset by the business is because the benefit in exchange for the payment is postponed to a future date. It stays an asset till the time the actual expense is due and recognized accordingly.

Such an expense has an unexpired value which means the benefit in exchange for the payment is still to be received. As a result, it is also called unexpired expense or unexpired cost.

Consider it a slow-burning asset that gradually becomes an expense and exhausts when the actual due date comes around.

Why is it considered a current asset?

Assets that are generally expected to be used, sold, or depleted within the current accounting year (usually 12 months) are called current assets.

The expectation around a prepaid expense is to convert it from being an asset to realising it as an income within a year.

Commonly a business expects to use, sell, or exhaust the current asset within the current accounting period therefore it is regarded as a current asset. In this way, they contribute to the calculation of the current ratio but they are excluded from the list of liquid assets.

In continuation of the previous heading, it is important to know that the prepaid expense is also shown as a reduction from the related direct or indirect expense in the Trading and P&L A/c.

Prepaid Expense is Which Type of Account?

As per the traditional classification of accounts, a prepaid expense is a type of personal account (representative personal). These types of accounts represent a person or a group.

It makes sense to call it a representative personal account since it’s indirectly linked to a person or group. As per the rules of debit and credit, it follows the rule of Dr. the receiver and Cr. the giver.

However, as per modern accounting rules, it is an asset and follows the rule of Dr. the increase and Cr. the decrease.

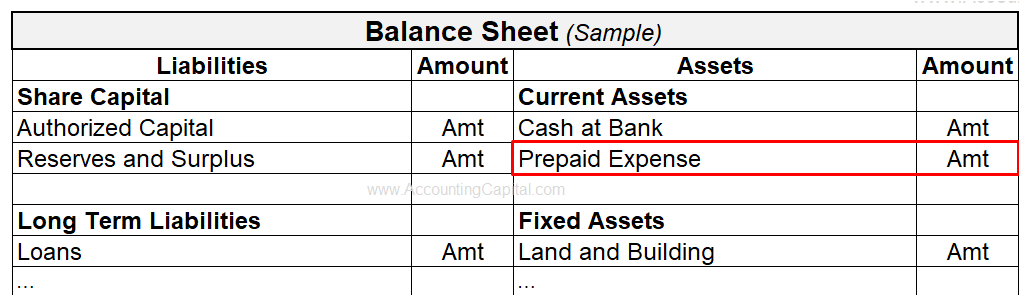

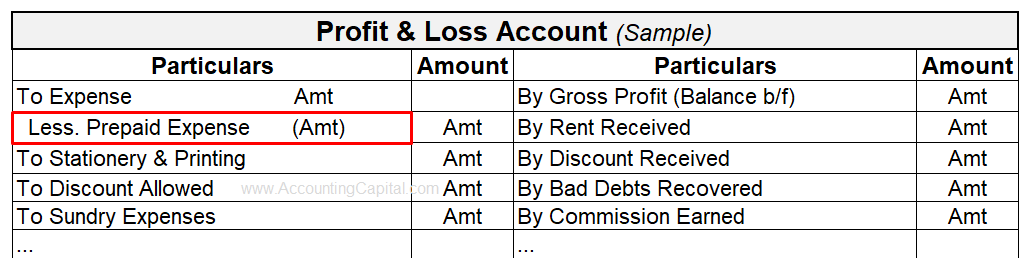

Treatment in Final Accounts

Treatment of Prepaid Expenses in Financial Statements/Final Accounts

Trading & Profit and Loss A/c Show on the Dr. side (subtract from the respective direct or indirect expense)

Balance Sheet: Show on the “Assets” side (under the head “Current Assets”)

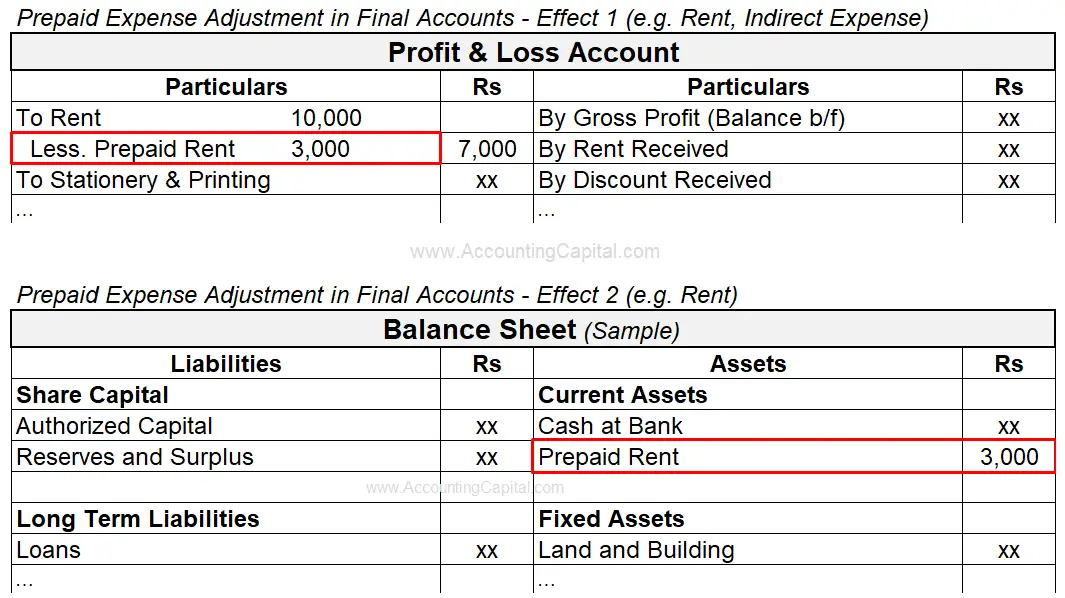

Example

In the year, a company paid Rs 10,000 in rent and estimated the prepaid rent to be Rs 3,000. Adjust prepaid expenses in final accounts at the end of the period.

Revision and Highlights

Highly Recommended!!

Do not miss our 1-minute revision video and the quiz below. This will help you quickly revise and memorize the topic forever. Try them :)

Short Quiz for Self-Evaluation

Loading

Your quiz has been submitted

Want to re-attempt? - Simply “refresh” this page.

Please check out more content on our site :)

Subscribed? - Check your mailbox

Thank You!

Server Side Error

We faced problems while connecting to the server or receiving data from the server. Please wait for a few seconds and try again.

If the problem persists, then check your internet connectivity. If all other sites open fine, then please contact the administrator of this website with the following information.

TextStatus: undefined HTTP Error: undefined

Processing you request

Error

Some error has occured.

Conclusion

Prepaid expenses are also referred to as deferrals, prepayments, deferred expenses, unexpired costs, prepaids, or prepaid liabilities. Some more common examples not shared above are interest expenses, estimated taxes, some utility bills,

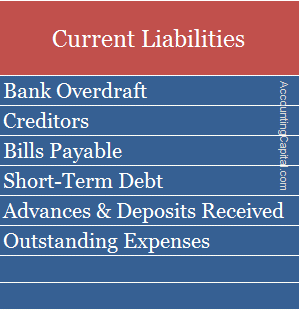

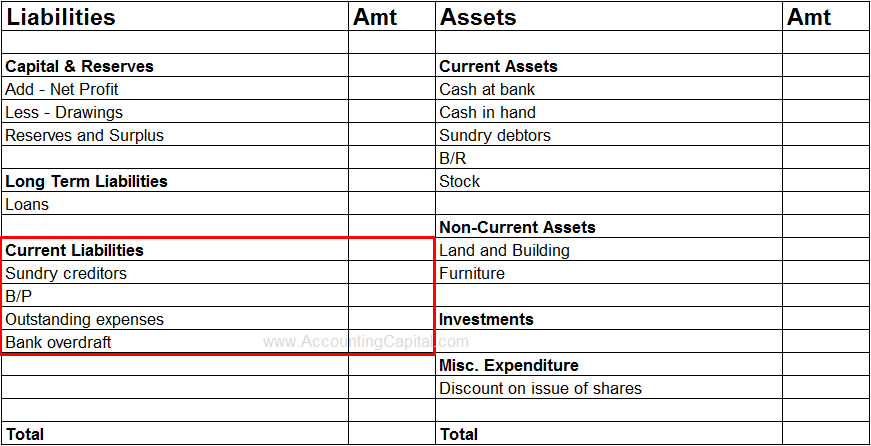

Obligations of a company which are payable within a year or an accounting cycle of a business are called current liabilities. They are either settled by current assets or by the introduction of new short-term liabilities.

Examples include Overdraft, Creditors, Short-term loans, Outstanding Expenses, etc. They are shown on the Liabilities side of the balance sheet.

They play a vital role in the control of the working capital of a business, WC = CA – CL, therefore, more of such short-term obligations mean less working capital and vice-versa.

It is also the denominator when looking at a company’s current ratio thus playing an important part in its liquidity. It is imperative to keep a check on such short-term liabilities.

Current Liabilities in Financial Statements

They are shown in the liabilities section of the balance sheet.

Short Quiz for Self-Evaluation

Loading

Your quiz has been submitted

Want to re-attempt? - Simply “refresh” this page.

Please check out more content on our site :)

Subscribed? - Check your mailbox

Thank You!

Server Side Error

We faced problems while connecting to the server or receiving data from the server. Please wait for a few seconds and try again.

If the problem persists, then check your internet connectivity. If all other sites open fine, then please contact the administrator of this website with the following information.

In the business world, a lot of sales transactions happen on credit, i.e. after a specified period of time. In this scenario, there are two main types of discounts allowed to customers. One is trade discount and the other is a cash discount.

Now, after anticipating the amount of cash discount allowable to debtors, a separate “provision for discount on debtors account” is opened and it is very similar to the “provision for doubtful debts account”. The only difference between the two is that provision for a discount is calculated on the debtors’ balance after deducting the provision for doubtful debts.

Journal Entry to Create Provision for Discount on Debtors

Profit & Loss A/C

Debit

To Provision for Discount on Debtors A/C

Credit

If a provision for discount on debtors exists at the time of providing the discount, then write off the discount from that provision.

A new provision should then be calculated to the extent of bringing the existing provision to the new figure. A journal entry would include debiting P&L account and crediting provision for discount on debtors.

If new provision required is lower than the provision already existent, then we need to transfer the difference to P&L account. In this case, the journal entry would be reverse of what is mentioned in the previous point.

Bad debts after trial balance, provision for doubtful debts and provision for discount on debtors will appear on the balance sheet as shown below;

Doubtful debts, as the name suggests, are those receivables which might become bad debts at some point in future. In other words, they are doubtful in recovery.

By analyzing the past trend, a business can ascertain the approximate percentage that becomes uncollectible every year out of the total credit allowed to buyers. This amount, thus estimated, is kept aside from the profits. This provision, made out of profits, is called Provision for Doubtful Debts.

Journal Entry to Create Provision for Doubtful Debts

Profit & Loss A/C

Debit

To Provision for Doubtful Debts

Credit

It is charged against the current year’s profits.

Provision for doubtful debts acts as a liability for the business and is shown on the liability side of a balance sheet. Every year the amount gets changed due to the provision made in the current year. Bad debts for the current year are to be set off, and an additional amount of provision is to be added.

When certain bad debts are to be written off and a provision for doubtful debts is to be made, the amount should be first debited against the existing balance of provision and the remaining balance in the account should be brought up to the required figure.

This can be easily understood as;

The calculation in the case where bad debts occurring in the following year have to be adjusted and an additional amount of provision is to be made, the calculation should be done in the following sequence:

=Bad debts (Add) New provision (Less) Old Provision

Sometimes earned revenue that belongs to a future accounting period is received in the current accounting period, such income is considered as income received in advance. It is also known as Unearned Revenue, Unearned Income, Income Received but not Earned because it is received before the related benefits are provided.

This revenue is not related to the current accounting period, for example, Rent received in advance, Commission received in advance, etc.

It is a personal account and is shown on the liability side of a balance sheet.

Journal Entry for Income Received in Advance

Income A/C

Debit

To Income Received in Advance A/C

Credit

Example

In March 10,000 were received in advance for rent which belonged to the month of April. The journal entry to record this in the current accounting period (31st March) will be as follows:

Rent Received A/C

10,000

To Rent Received in Advance A/C

10,000

Treatment in the Financial Statements

Following is how income received in advance is treated in the final accounts and how it is shown in both the Profit and Loss Account and the balance sheet.

Reduction from the concerned income on the credit side of the income statement.

Do not miss our 1-minute revision video and the quiz below. This will help you quickly revise and memorize the topic forever. Try them :)

Short Quiz for Self-Evaluation

Loading

Your quiz has been submitted

Want to re-attempt? - Simply “refresh” this page.

Please check out more content on our site :)

Subscribed? - Check your mailbox

Thank You!

Server Side Error

We faced problems while connecting to the server or receiving data from the server. Please wait for a few seconds and try again.

If the problem persists, then check your internet connectivity. If all other sites open fine, then please contact the administrator of this website with the following information.

Profit Center is a section of a company that is treated as a separate sub-business within a company to which revenues can be traced. It directly adds to the profits of the company, hence it is responsible for its own costs and revenues.

Each profit centre or a few are managed by profit centre managers who are responsible for their own centers. This helps organizations to compare different profit centers and determine which ones need more attention and are earning fewer profits, etc.

Profit centers may be divisions, subsidiaries or departments. Results of profit centers are generally included in externally reported segment results.

Example

Asset management department (for an asset management company), Sales department, Advice & Wealth Management (for a wealth management company) etc.

Total of AWM will be total of all it sub profit centers

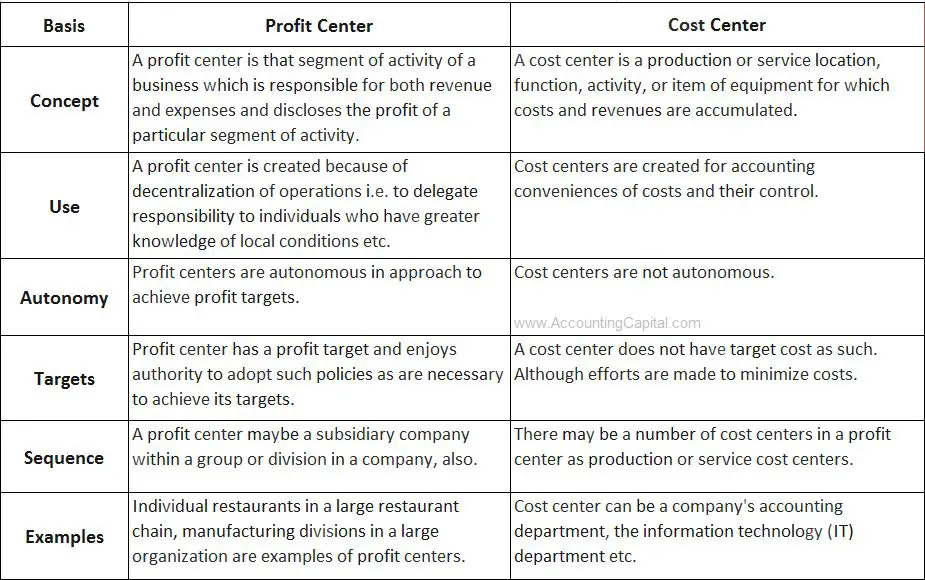

Profit Center and Cost Center

A profit center is that part of the activity of a business that is considered responsible for earning revenue and incurring expenses and also establishes the profit of a particular segment of activity. Profit centers are maintained to measure the performance of each individual to whom the responsibility was delegated.

A cost center is the smallest unit in an operational organization for which distinct cost collection and analysis is attempted. A cost center can be defined as an observable unit in a big organization, that is established for the convenience of cost detection.

Difference in Table Format

Why is the Profit Center important?

Managerial accounting mainly focuses on identifying the sources of profits in a business. This leads to accumulating the revenue generated and the expenses incurred in respect of these sources of profit.

Most organizations depend on the traditional income statement that shows the overall profit and cost for the whole business. The real problems and opportunities can be explored only with granular information.

Profit centers can help a business earn a superior return on its investments given the utilization of its limited resources in comparison with alternative opportunities available to it, with help of profit comparison.

Many businesses try to capture new markets by pricing their products and services too low. Price is very crucial in the absence of value. Charging prices below the required profit renders the business unsustainable. Hence, a grasp on expected profit levels is very much required.

Profit centers promote healthy competition among different units of the same business. The aim is to allow a microscopic view of the observable units of the business to establish how each of these units is performing financially, in terms of profitability.

Profit centers increase the profit consciousness of the business leading to overall enhanced profitability of the organization.

Problems with Profit Centers

There are reasons for a business to establish profit centers but, the process may lead to some difficulties also:

Profit Centers can lead to decentralization. But, decentralized decision making may force the top management to rely further upon the mid-management reports. This leads to a loss of control.

Divisionalization can lead to additional costs because of the additional required management controls, staff, and record-keeping resources.

An excess of Profit consciousness may result in overemphasis on short-run profitability at the expense of long-run sustainable growth.

There is no completely functional system in place yet, to ensure that divisional profit will contribute to the overall organizational growth or not.

There has to be a check on the level and nature of competition budding among different profit centers of the same business.

Short Quiz for Self-Evaluation

Loading

Your quiz has been submitted

Want to re-attempt? - “Refresh” this page.

Check out more content on our site :)

Subscribed? - Check your mailbox

Thank You!

Server Side Error

We faced problems while connecting to the server or receiving data from the server. Please wait for a few seconds and try again.

If the problem persists, then check your internet connectivity. If all other sites open fine, then please contact the administrator of this website with the following information.

A function or department in the organization that does not directly add to the profit, but costs the organization money to operate is known as a cost center. The cost center indirectly adds to the profitability of the business.

The cost center operates on a budget decided by the organization. By showcasing operational excellence, the cost centers manage to keep a check on the costs incurred by them and stick to the budgetary restrictions.

The cost centers do not involve themselves in the investment or revenue decisions of an organization. Their main function is to track expenses. This allows for more accurate budgets and forecasts. The data that they provide is basically for internal reporting. The management can use the data provided by cost centers to improve operational efficiency and maximize profits.

Some cost centers observed in organizations are:

Accounting Department

IT Department

HR Department

Quality Control Department (in case of manufacturing units)

Maintenance Staff

Example

Human Resources department, Finance department, etc.

The total of HR will be the total of all its sub cost centers.

Similarly, for the Research & Development department, it incurs lots of costs in its endeavor to come up with new products for the company, though it is difficult to say how much profit it generates for the company. The sum of Research, Planning, and Implementation of new plans will be the total for this department.

Uses

A cost center is used to track expenditure for a specific function. Without creating such a cost center, it would take immense effort to measure the cost of supplying this service exactly. It would require breaking up of all expenditures of the business department wise, which is a very tedious task.

It is also used to allocate resources to the most profitable activities as this requires to track costs for all activities undertaken.

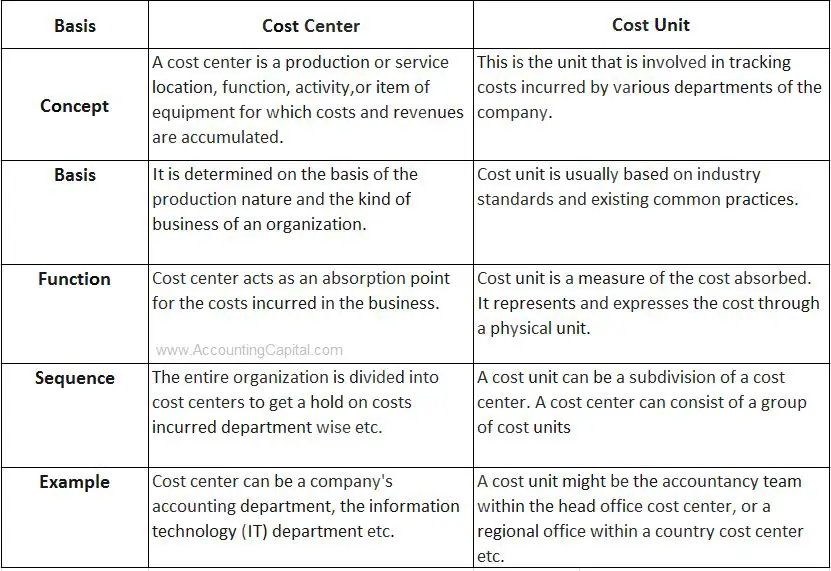

Cost Unit and Cost Center

Cost Unit

It is a representing unit of product, service, or time (can be a combination of these) in respect to which costs may be ascertained, collected, or expressed. For instance, a business may like to determine the cost per tonne of steel, per tonne-kilometre of a transport service, or cost per machine hour.

A single contract/project can also be a cost unit

A batch/group of identical items that maintains its identity through one or more stages of production can also be a cost unit

Cost units are usually units of physical measurement such as area, volume, weight, value, number, or time

Example

A brick-making company ascertains its cost per 1,000 bricks.

An electricity production company measures its cost per kilowatt-hour(kwh).

A hospitality business determines its cost of maintenance per room.

A transport business ascertains its cost incurred per passenger kilometre.

These are the cost units for the above-mentioned businesses and include parameters of physical measurement.

Differences

Sometimes, cost center and cost unit act as one, but they have clear distinguishable characteristics:

Types of Cost Centers

Following is the broad classification of cost centers, observed in an organization:

Personal CC

A personal cost center refers to a person or a group of people. For example, a sales manager, a workforce manager, etc.

Impersonal CC

The impersonal cost center refers to a location, equipment, a group of these, or both. For example, the London branch, boiling house, cooling tower, the generator set, etc.

Production CC

A production cost center is associated with a product or manufacturing work. It is a cost center where the raw material is handled for conversion into finished products. Here both direct and indirect expenses are incurred. For example, machine shops, welding shops, and assembly shops, etc.

Service CC

A service cost center involves providing services to the production department. It serves as an ancillary unit to a production cost center. For example, payroll processing department, powerhouse, service centers, plant maintenance centers, etc.

Short Quiz for Self-Evaluation

Loading

Your quiz has been submitted

Want to re-attempt? - “Refresh” this page.

Check out more content on our site :)

Subscribed? - Check your mailbox

Thank You!

Server Side Error

We faced problems while connecting to the server or receiving data from the server. Please wait for a few seconds and try again.

If the problem persists, then check your internet connectivity. If all other sites open fine, then please contact the administrator of this website with the following information.

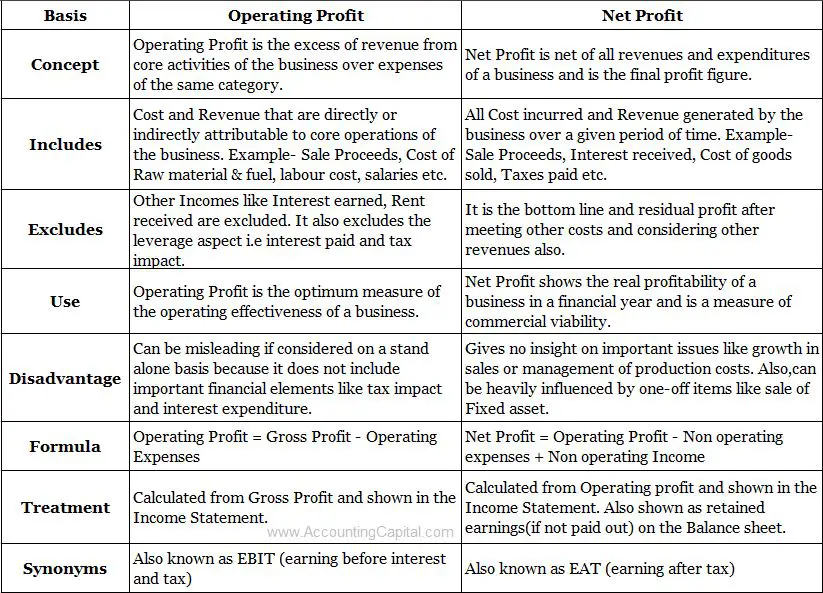

The term “profit” is divided into different types according to the source of benefit and the stage at which it is calculated during the life cycle of a business. This article illustrates the difference between net profit and operating profit.

Some of the most common forms of profit that can be found in financial statements are gross profit, net profit, operating profit, etc. All of them are calculated for different reasons, and each plays a diverse role in their journey through the accounting cycle.

Net Profit

The word Net means “after all deductions”. Accordingly, the profit earned after all deductions is called Net Profit. It is also called Net Income or Net Earnings. It is the difference between “total revenue earned” and “total cost incurred”.

Deductions include adjustments related to the cost of doing business, such as taxes, depreciation and other miscellaneous expenses.

Net Profit = Total Revenue – Total Cost

Net Profit = Gross Profit – (Total expenses from operations, interests and taxes)

Net profit can be found on a company’s income statement & it is further transferred to the organization’s balance sheet. (Add to capital)

Profit earned from a firm’s core business operations is called Operating Profit. So a shoe company’s operating profit will be the profit earned only from selling shoes. Operating profit doesn’t include any profits earned from investments and interests. It is also known as Operating Income, PBIT and EBIT (Earnings before Interest and Taxes).

It is the excess of Gross Profit over Operating Expenses.

One of the main points of difference between net profit and operating profit is that net profit takes into account earnings from all sources & all sorts of deductions. In contrast, operating profit only considers profits earned from operations.

The difference in Table Format

A few more differences are;

Net profit is often used by investors and analysts to evaluate a company’s overall financial performance.

Operating profit is often used by managers to identify areas for improvement in a company’s operations.

Net profit is affected by a company’s financial decisions, such as borrowing money or paying dividends.

Operating profit is not affected by these financial decisions.

Short Quiz for Self-Evaluation

Loading

Your quiz has been submitted

Want to re-attempt? - Simply “refresh” this page.

Please check out more content on our site :)

Subscribed? - Check your mailbox

Thank You!

Server Side Error

We faced problems while connecting to the server or receiving data from the server. Please wait for a few seconds and try again.

If the problem persists, then check your internet connectivity. If all other sites open fine, then please contact the administrator of this website with the following information.

The word Gross means “before any deductions”. This implies that profit before any deductions is called Gross profit. It is also called “Sales Profit”. Difference between gross profit and operating profit can be understood from their point of origin, deductions (if any), etc.

It is the difference between total revenue earned from selling products/services and total cost of goods/services sold.

The profit earned from a firm’s core business operations is called Operating profit. So, a shoe company’s operating profit will be the profit earned from only selling shoes.

The Operating profit doesn’t include any profits earned from investments and interests. It is also known as “Operating Income”, “PBIT” (Profit before Interest and Taxes) and “EBIT” (Earnings before Interest and Taxes).

It is the excess of Gross Profit over Operating Expenses.

*Any other profit earned from different sources, except operations of the business, will not be included to calculate the operating profit.

One of the main points of difference between gross profit and operating profit is that gross profit takes into account earnings from all sources whereas operating profit only considers profits earned from operations.

Short Quiz for Self-Evaluation

Loading

Your quiz has been submitted

Want to re-attempt? - Simply “refresh” this page.

Please check out more content on our site :)

Subscribed? - Check your mailbox

Thank You!

Server Side Error

We faced problems while connecting to the server or receiving data from the server. Please wait for a few seconds and try again.

If the problem persists, then check your internet connectivity. If all other sites open fine, then please contact the administrator of this website with the following information.

The difference between cost and management accounting is very important to understand as both of them serve different purposes and different audiences.

A person from the cost accounting team may not find a piece of information relevant, but a management accountant may not be able to work without it. A cost accountant and a manager would need different sets of information from the accounting records of a business.

Cost Accounting

It is the branch of accounting which is mainly concerned with “Cost aspect of accounting”. Cost accounting intends to capture and competently manage a company’s costs of production by examining and evaluating various alternative courses of action.

The main goal of cost accounting is to find out the cost of production or services rendered and use this information to evaluate the profitability and efficiency of business operations. The most appropriate course of action is sought based on ability and cost-efficiency.

It considers both past and present numbers in the process of evaluation.

Example: Let’s assume that an FMCG company has decided to introduce a new product in their range, they will need cost accounting information, such as the cost of production per unit, to price the product correctly in the market.

Management Accounting

It helps in effective performance management, control, planning, decision-making, etc. It generally includes budgeting decisions as well. Since management accounting is not a legal requirement, it is not based on Generally Accepted Accounting Principles and accounting standards.

It is the branch of accounting, which is mainly concerned with “Internal users of information”, commonly – the managers. Management accounting provides a basis to the internal users to make a logical and informed decision.

It focuses mainly on the future and concerned with future projections.

Example: Let’s assume that a Sr. Manager wants to make an internal decision on an investment made in a particular business segment. It will need internal management accounting data such as the return on investment, etc.

The above mentioned are a few key points of difference between the cost accounting and the management accounting.

Short Quiz for Self-Evaluation

Loading

Your quiz has been submitted

Want to re-attempt? - Simply “refresh” this page.

Please check out more content on our site :)

Subscribed? - Check your mailbox

Thank You!

Server Side Error

We faced problems while connecting to the server or receiving data from the server. Please wait for a few seconds and try again.

If the problem persists, then check your internet connectivity. If all other sites open fine, then please contact the administrator of this website with the following information.

The difference between financial accounting and cost accounting is very important to understand as both of them serve different purpose and audience.

A person from the management may not find certain information relevant, and at the same time, a cost accountant can’t work without this information. A creditor and a cost accountant would need different sets of information from the accounting records of a business.

Financial Accounting

It is a branch of accounting, which deals with classifying, measuring and recording a business transaction. Financial accounting is concerned with the preparation of financial statements for the purpose of demonstrating the performance and position of a business. The end products are P&L Account for the period end and Balance Sheet as on the last day of the accounting period.

It is mainly concerned with the “External users of information” such as Shareholders, Government, Lenders, Public and other users of accounting information.

It focuses on the history and historical records.

Example: Suppose a Bank wants to decide whether to extend credit to a firm. It will need to look into the business’ financial accounting data such as financial statements.

It is the branch of accounting, which is mainly concerned with “Cost aspect of accounting”. Cost accounting intends to capture and competently manage a company’s cost of production by examining and evaluating various alternative courses of action.

The main goal of cost accounting is to find out the cost of products or services rendered and use this information to evaluate the profitability and efficiency of business operations. The most appropriate course of action is developed based on ability and cost-efficiency.

It considers both past and present numbers during the evaluation process.

Example: Let’s say that an FMCG company has decided to introduce a new product in their range; they will need cost accounting information such as the cost of production per unit, etc. to price the product correctly in the market.

The above information presents a few key points of difference between financial accounting and cost accounting.

Short Quiz for Sef-Evaluation

Loading

Your quiz has been submitted

Want to re-attempt? - Simply “refresh” this page.

Please check out more content on our site :)

Subscribed? - Check your mailbox

Thank You!

Server Side Error

We faced problems while connecting to the server or receiving data from the server. Please wait for a few seconds and try again.

If the problem persists, then check your internet connectivity. If all other sites open fine, then please contact the administrator of this website with the following information.

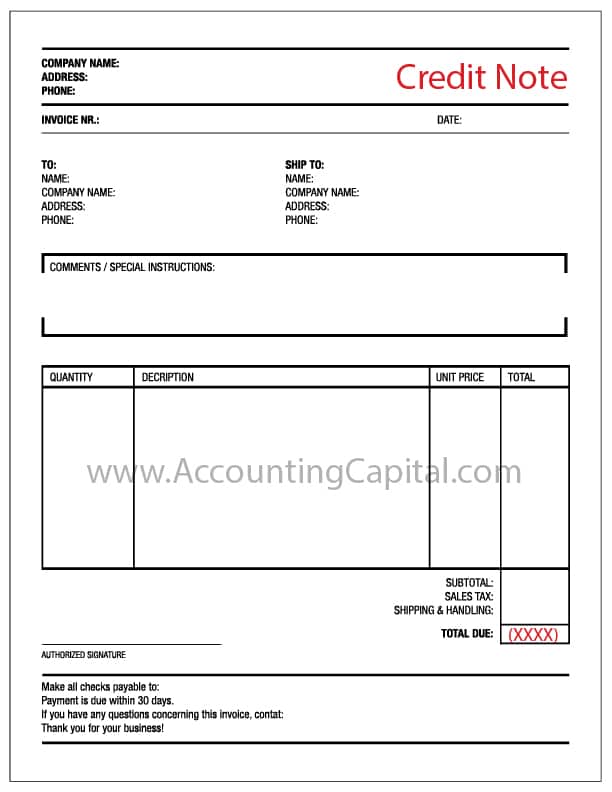

When a customer returns goods purchased on credit he/she also expects some form of confirmation from the seller along with the cancellation of related dues. A credit note is a documentsent by a seller to the buyer as a notification to acknowledge that the goods have been registered as “returned” (return inwards) and a credit has been provided to them for the eligible amount.

In other words, it is a commercial document issued by a seller to the buyer. It acts as evidence of sales returns and a reduction of the amount owed by the buyer for an invoice raised earlier. A credit note is also called a “credit memo”.

It reduces the amount due to be paid by the customer, if the amount due is nil then it allows further purchases in lieu of the credit note itself.

A credit note is issued for the value of goods returned by the customer, it may be less than or equal to the total amount of the order.

Example of Credit Note

Company B purchases goods worth 1,00,000 from Amazon in a (business to business) transaction, however, 10,000 worth of goods were found damaged due to some reason & this was notified to Amazon at the time of actual delivery.

Amazon (seller) issues a credit note for 10,000 in the name of Company-B (buyer). This reduces the accounts receivable for Amazon by 10,000 and the buyer is only required to pay 90,000.

Important Characteristics

1. It is sent to inform about the credit made in the account of the buyer along with the reasons.

2. The sales return book is updated on its basis. (In case of return of goods)

3. Usual reasons range from goods found incomplete, damaged, inaccurate goods sent, etc.

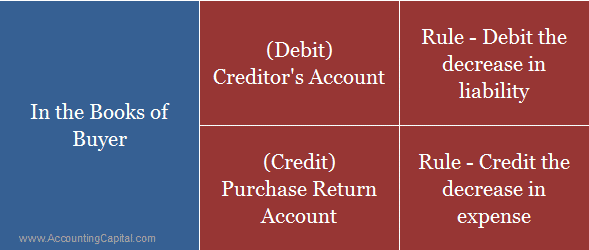

Goods returned are purchase returns for the buyer, this action leads to the following;

A decrease in liability to pay the respective creditor.

A decrease in expense previously incurred to purchase goods.

Creditor’s A/C

Debit

To Purchase Return A/C

Credit

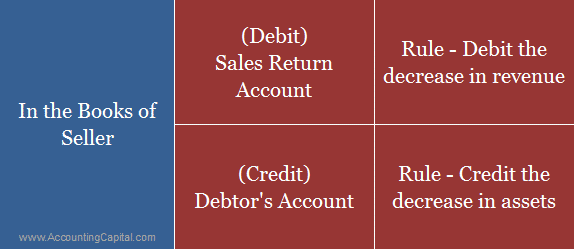

In the books of seller

Goods received as returned are sales return for the seller, this action leads to the following;

A decrease in revenue previously booked as sales.

A decrease in assets as money will not be received from the debtor anymore.

Sales Return A/C

Debit

To Debtor’s A/C

Credit

Sample Credit Note Template

Revision and Highlights

Highly Recommended!!

Do not miss our 1-minute revision video and the quiz below. This will help you quickly revise and memorize the topic forever. Try them :)

Short Quiz for Self-Evaluation

Loading

Your quiz has been submitted

Want to re-attempt? - Simply “refresh” this page.

Please check out more content on our site :)

Subscribed? - Check your mailbox

Thank You!

Server Side Error

We faced problems while connecting to the server or receiving data from the server. Please wait for a few seconds and try again.

If the problem persists, then check your internet connectivity. If all other sites open fine, then please contact the administrator of this website with the following information.

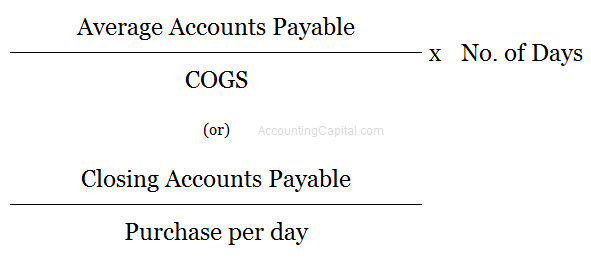

Days payable outstanding or DPO is the average number of days that a company takes to pay its outstanding suppliers after a credit purchase has been recorded.

It is used for the estimation of an average payment period and helps to determine the efficiency with which the company’s accounts payable are being managed.

Days payable outstanding or DPO is usually a monthly activity and it may fluctuate every month. This can be due to multiple business scenarios such as seasonality, change in business policies, economics, etc.

It is useful for preserving working capital, however, while preserving the working capital a company also needs to ensure that all payments to its suppliers are done within the due date. Monitoring the DPO enables the management to ensure that cash is utilized optimally and the payment terms with creditors are maintained.

Formula to Calculate Days Payable Outstanding (DPO)

DPO can be expressed in either way

LOW DPO – The company is taking less number of days to pay back to its suppliers. This is usually a sign of good financial health.

HIGH DPO – The company is taking more number of days to pay back to its suppliers. This may be done temporarily as a strategic decision or it may be a result of week liquidity of the company.

It means the average number of days that the company takes to pay its invoices is 3 days.

Short Quiz for Self-Evaluation

Loading

Your quiz has been submitted

Want to re-attempt? - “Refresh” this page.

Check out more content on our site :)

Subscribed? - Check your mailbox

Thank You!

Server Side Error

We faced problems while connecting to the server or receiving data from the server. Please wait for a few seconds and try again.

If the problem persists, then check your internet connectivity. If all other sites open fine, then please contact the administrator of this website with the following information.

In its simplest form, capital means the funds brought in to start a business by the owner(s) of a company. It is an investment by the proprietor(s) or partner(s) in the business. Bringing equity into a business can mean money or assets as well. It is business’ liability towards the owner(s) also referred to as one of the internal liabilities of the business. It is also called Net Worth or Owner’s Equity.

Examples include vehicles, patents, buildings, etc.

It can increase with fresh investments or profits earned by the business.

It can decrease with drawings made by the owner(s) or losses incurred by the business.

What Type of an Account is Capital and Where is it Shown in Financial Statements?

It is a liability for the business and, according to the traditional classification of accounts, it is a Personal A/C. Capital is shown on the “Liability” (left hand) side of a balance sheet.

Short Quiz for Self-Evaluation

Loading

Your quiz has been submitted

Want to re-attempt? - “Refresh” this page.

Check out more content on our site :)

Subscribed? - Check your mailbox

Thank You!

Server Side Error

We faced problems while connecting to the server or receiving data from the server. Please wait for a few seconds and try again.

If the problem persists, then check your internet connectivity. If all other sites open fine, then please contact the administrator of this website with the following information.

A service center is an organizational unit which provides services to other departments within an organization. Its main task is to serve other departments within the organization, such as other service centers, cost centers and profit centers. A service center can be further divided into sub service centers.

Example

Technology department, Real Estate department, etc.

Total of Technology will be total of all its sub service centers

Nowadays, businesses sell their assets as part of strategic decision-making. Sale of an asset may be done to retire an asset, funds generation, etc. Such a sale may result in a profit or loss for the business. In the case of profits, a journal entry for profit on sale of fixed assets is booked.

It is very common that an asset may not be sold at current book value, hence if it is sold for more than its written down value it generates profit for the business and in a situation opposite to that i.e. when it is sold for less it incurs a loss.

Loss or profit on the sale of an asset is to be shown on the appropriate side of the profit and loss account.

There are 3 different accounts that will be affected in this case;

Asset being sold

Cash being received

Profit earned on the sale of an asset

Journal Entry for Profit on Sale of Fixed Assets

Cash A/c

Debit

Real Account

Debit what comes in

To Sale of Asset

Credit

Real Account

Credit what goes out

To Profit on Sale of Asset

Credit

Nominal Account

Credit all gains

Short Quiz for Self-Evaluation

Loading

Your quiz has been submitted

Want to re-attempt? - Simply “refresh” this page.

Please check out more content on our site :)

Subscribed? - Check your mailbox

Thank You!

Server Side Error

We faced problems while connecting to the server or receiving data from the server. Please wait for a few seconds and try again.

If the problem persists, then check your internet connectivity. If all other sites open fine, then please contact the administrator of this website with the following information.

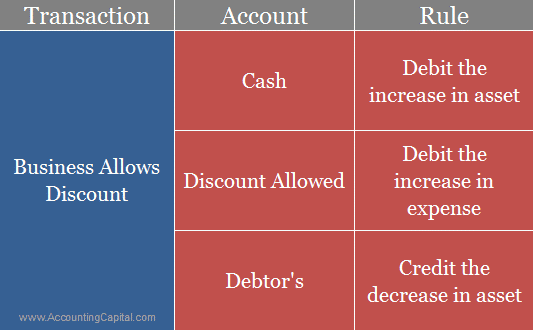

Discounts are very common in today’s business world, they are generally provided in lieu of some consideration which can range from timely payments to market competition. While posting a journal entry for discount allowed “Discount Allowed Account” is debited.

Discount allowed acts as an additional expense for the business and it is shown on the debit side of a profit and loss account. Trade discount is not shown in the main financial statements, however, cash discount and other types of discounts are supposed to be recorded in the books of accounts.

In case of a transaction where both trade discount and cash discount are allowed, the trade discount is allowed first and then the cash discount is processed.

Discount allowed by a seller is discount received for the buyer. The following examples explain the use of journal entry for discount allowed in real-world events.

Examples – Journal Entry for Discount Allowed

Cash received for goods sold to Unreal Co. worth 50,000 along with a 10% discount. (Discount allowed in the regular course of business)

Cash A/C

45,000

Discount Allowed A/C

5,000

To Unreal Co. A/C

50,000

Received 5,000 from Unreal Co. in full and final settlement of their account worth 10,000. (Discount allowed to settle an overdue payment)

Cash A/C

5,000

Discount Allowed A/C

5,000

To Unreal Co. A/C

10,000

Short Quiz for Self-Evaluation

Loading

Your quiz has been submitted

Want to re-attempt? – “Refresh” this page.

Check out more content on our site :)

Subscribed? – Check your mailbox

Thank You!

Server Side Error

We faced problems while connecting to the server or receiving data from the server. Please wait for a few seconds and try again.

If the problem persists, then check your internet connectivity. If all other sites open fine, then please contact the administrator of this website with the following information.

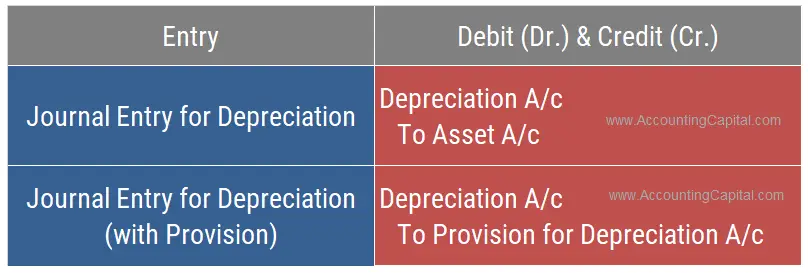

A reduction in the value of tangible fixed assets due to normal usage, wear and tear, new technology or unfavourable market conditions is called Depreciation. Whether you maintain the provision for depreciation/accumulated depreciation account determines how to do the journal entry for depreciation.

Assets such as plant and machinery, buildings, vehicles, furniture, etc., expected to last more than one year but not for an infinite number of years, are subject to depreciation.

In the books of accounts, depreciation can be recorded by any of the following two methods,

1. When depreciation is charged to the ‘Asset’ account.

2. When provision for depreciation/accumulated depreciation is maintained.

More often than not, the second method is used.

Method 1 – Depreciation Charged to the Asset Account

In this method, the asset account is charged (credited) with depreciation. There is one disadvantage of this method, which is that it is not possible to find out the original cost of an asset and the total amount of depreciation.

Depreciation A/c

Debit

To Asset A/c

Credit

(Depreciation charged directly to the fixed asset)

Accounting rules applied in the above journal entry are;

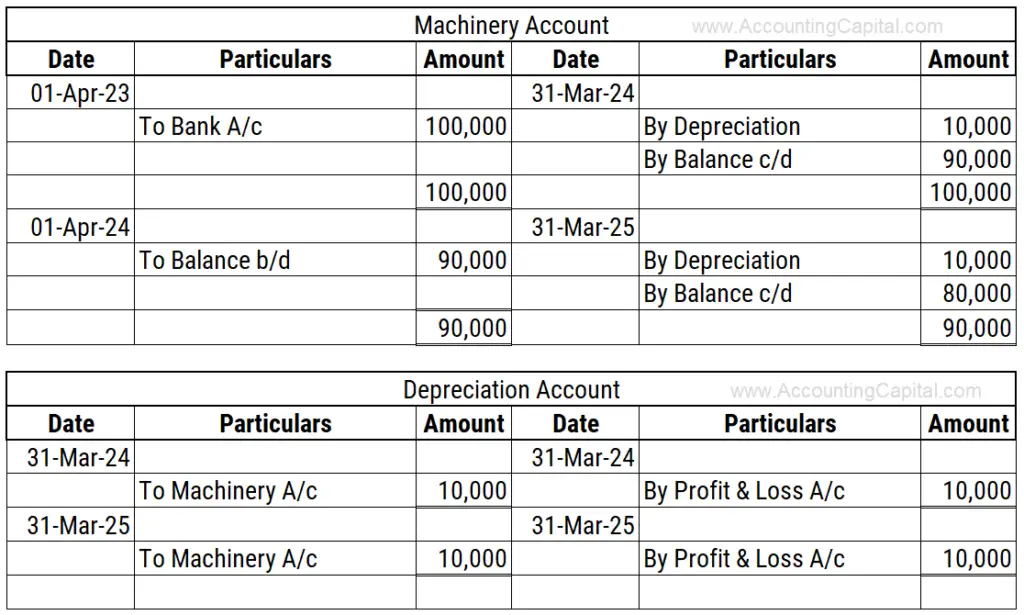

(Being depreciation charged transferred to profit & loss account)

After the asset’s useful life is over and when all depreciation is charged, the asset approaches its scrap or residual value.

Method 2 – Entry when Provision for Depreciation or Accumulated Depreciation Account is Maintained

When using this method, depreciation is not credited to the asset account. A provision for depreciation or an accumulated depreciation account is maintained where depreciation is credited separately.

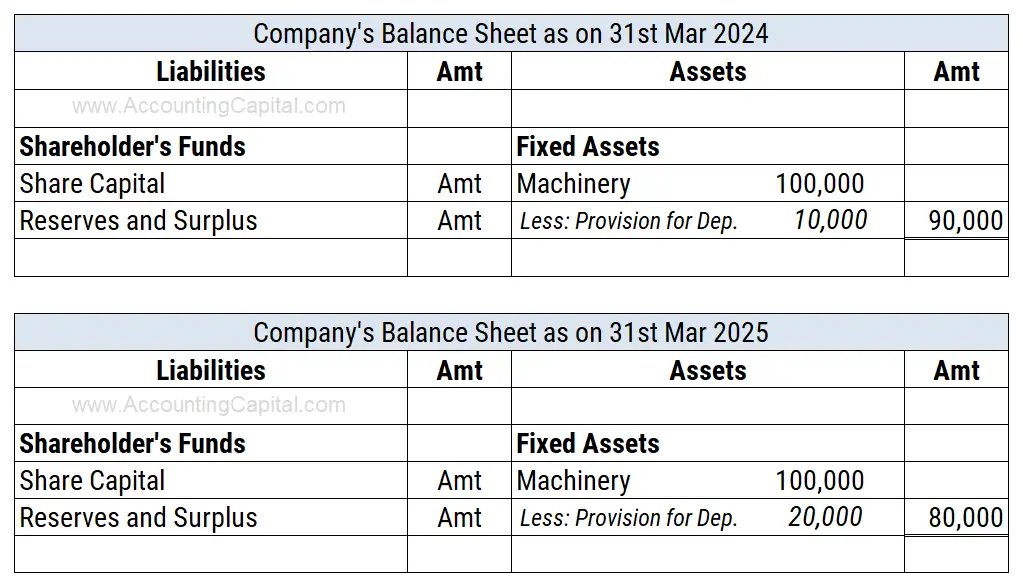

As a result of this method, the asset can be shown at its original cost, and the provision for depreciation (contra account) can be shown on the liabilities side. It helps counterbalance.

It is also possible to deduct the accumulated depreciation from the asset’s cost and show the balance on the balance sheet.

Depreciation A/c

Debit

To Provision for Depreciation A/c

Credit

(Being depreciation charged accumulated in a separate account for the asset)

To Transfer Depreciation into P&L

Profit & Loss A/c

Debit

To Depreciation A/c

Credit

(Being depreciation charged transferred to profit and loss account)

Depreciation accumulated over the life of an asset is shown in the accumulated depreciation account.

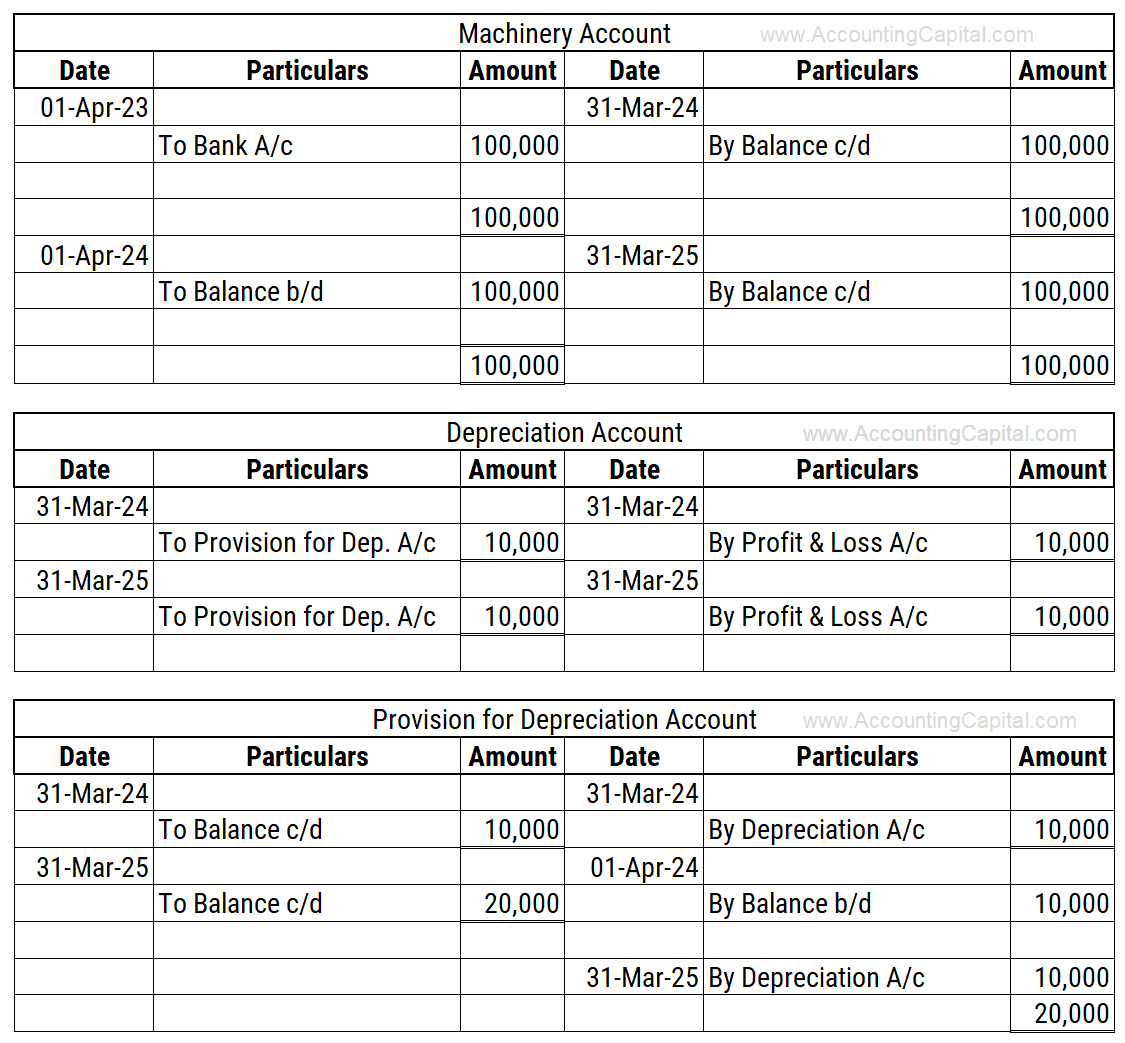

Let’s assume that a piece of machinery worth 100,000 was purchased on April 1st 2023, with a scrap value of nil and a depreciation rate of 10% (straight-line method). The company will close its accounts on 31st March.

Show entries for depreciation, all relevant accounts, and the company’s balance sheet for the next 2 years using both methods.

Method 1 – When no provision is maintained

31 Mar 2024 (end of year 1) – Depreciation charged on machinery

Depreciation A/c

10,000

To Machinery A/c

10,000

(Being depreciation charged on the machine @ 10% for year 1 SLM)

31 Mar 2025 (end of year 2) – Depreciation charged on machinery

Depreciation A/c

10,000

To Machinery A/c

10,000

(Being depreciation charged on the machine @ 10% for year 2 SLM)

Machinery A/c & Depreciation A/c for the next two years

Balance Sheet for the next two years (extract)

Method 2 – When provision for depreciation is maintained

Machinery A/c & Depreciation A/c for the next two years

Office furniture is subject to depreciation. Depending on the local laws, fittings may also be included in the definition of ‘furniture’.

This may include wiring, switches, sockets, light fittings, fans, and other electrical fittings. Every country’s regulatory bodies determine how furniture and fittings are depreciated.

Entry to depreciate office furniture,

Depreciation A/c

Debit

To Furniture A/c

Credit

(Assuming no provision/accumulated depreciation account is maintained)

The rules applied while charging depreciation on office furniture are,

Depreciation – Dr. the increase in depreciation expense.

Furniture – Cr. decrease in furniture value, which is an asset for the firm.

An expenditure directly related to making a machine operational and improving its output is considered a capital expenditure. In other words, this is a part of the machine cost that can be depreciated. For example, installation, wages paid to install, freight, upgrades, etc.

Entry to depreciate machinery,

Depreciation A/c

Debit

To Machinery A/c

Credit

(Assuming no provision/accumulated depreciation account is maintained)

The rules applied while charging depreciation on machinery are,

Depreciation – Dr. the increase in depreciation expense.

Furniture – Cr. decrease in machine’s value, which is an asset for the firm. In this case, it is important to add any capital expenditure incurred on the machinery’s cost.

When an asset is purchased, any expenses incurred on the purchase of the asset (except for goods) increase its cost. They are debited to the “Asset A/c” and not recognised as expenses.

It is important to note that all expenses incurred for the construction of the building are added to the cost of the building. These include purchasing construction materials, wages for workers, engineering, etc.

Entry to depreciate building,

Depreciation A/c

Debit

To Building A/c

Credit

(Assuming no provision/accumulated depreciation account is maintained)

The rules applied while charging depreciation on machinery are,

Depreciation – Dr. the increase in depreciation expense.

Furniture – Cr. decrease in machine’s value, which is an asset for the firm. In this case, it is important to add any capital expenditure incurred on the machinery’s cost.

Sometimes referred to as PPE (Property, Plant & Equipment), they are physical items held for use to operate a business. They are intended for use beyond 12 months.

Spare parts, stand-by equipment, and servicing equipment are not considered to be PPE unless they comply with the standards defining the term. In the absence of such items, they are considered inventory.

Entry to depreciate equipment is,

Depreciation A/c

Debit

To Furniture A/c

Credit

(Assuming no provision/accumulated depreciation account is maintained)

The rules applied while charging depreciation on office furniture are,

Depreciation – Dr. the increase in depreciation expense.

Furniture – Cr. decrease in furniture value, which is an asset for the firm.

Due to the fact that there is no estimated useful life associated with this asset, the land is not depreciated. It is not because “it is always appreciated”. In fact, in exceptional scenarios, land may depreciate as well. For these reasons, there is no journal entry for depreciation on land.

We faced problems while connecting to the server or receiving data from the server. Please wait for a few seconds and try again.

If the problem persists, then check your internet connectivity. If all other sites open fine, then please contact the administrator of this website with the following information.

Also known as unearned income, it is income which is received in advance, however, the related benefits are yet to be provided. It belongs to a future accounting period and is still to be earned. Journal entry for income received in advance recognizes the accounting rule of “Credit the increase in liability”.

Examples of income received in advance – Commission received in advance, rent received in advance, etc. Such advances received are treated as a liability for the business.

Journal entry for income received in advance is;

Income A/C

Debit

Debit the decrease in income

To Income Received in Advance A/C

Credit

Credit the increase in liability

As per accrual-based accounting unearned income must be recorded in the books of finance irrespective of when the related goods/services are provided.

Question – On December 20th 2019 Company-A receives 1,20,000 (10,000 x 12 months) as rent in cash which belongs to the following year (Jan 2020 to December 2020).

Show all related rent entries including journal entry for income received in advance on these dates;

December 20th 2019 (Same Day)

December 31st 2019 (End of the period adjustment)

January 1st 2020 to December 31st 2020 (Beginning of each month next year)

1. December 20th 2019 – (Money received for rent to be collected next year)

Cash A/c

1,20,000

To Rent Received A/c

1,20,000

2. December 31st 2019 – (Rent receivable next year adjusted with rent received in advance account)

Rent Received A/c

1,20,000

To Rent Received in Advance A/c

1,20,000

3. January 1st 2020 to December 1st 2020 – (Income matched to each period)

Rent Received in Advance A/c

10,000

To Rent Received A/c

10,000

All 12 months from Jan’20 to Dec’20 will be consumed in each period against the rent received in advance account to reduce the advance account to zero by end of the year.

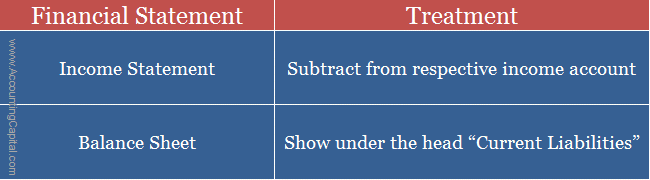

Treatment of Income Received in Advance in the Financial Statements

After posting the journal entry for income received in advance a business records it the final accounts as follows;

Reduces it from the concerned income head on the credit side of the income statement.

Treatment of income received in advance in the books of finance

Example – Journal Entry for Rent Received in Advance

Let’s assume that in the month of March 10,000 are received in advance for rent, the rent actually belongs to the month of April.

Journal entry to record this in the current accounting period is;

Rent Received A/c

10,000

To Rent Received in Advance A/c

10,000

(Assuming cash was debited and rent received was credited at the time of actual receipt)

Example – Journal Entry for Commission Received in Advance

Total of 2000 was received as commission earned in the current accounting year. Post the journal entry for income received in advance (commission earned) to include the impact of this activity.

Commission Received A/c

2,000

To Commission Received in Advance A/c

2,000

(Assuming cash was debited and commission received was credited at the time of actual receipt)

Short Quiz for Self-Evaluation

Loading

Your quiz has been submitted

Want to re-attempt? – “Refresh” this page.

Check out more content on our site :)

Subscribed? – Check your mailbox

Thank You!

Server Side Error

We faced problems while connecting to the server or receiving data from the server. Please wait for a few seconds and try again.

If the problem persists, then check your internet connectivity. If all other sites open fine, then please contact the administrator of this website with the following information.

It is income earned during a particular accounting period but not received until the end of that period. It is treated as an asset for the business. Journal entry for accrued income recognizes the accounting rule of “Debit the increase in assets” (modern rules of accounting).

Examples of accrued income – Interest on investment earned but not received, rent earned but not collected, commission due but not received, etc.

Journal entry for accrued income is;

Accrued Income A/C

Debit

Debit the increase in asset

To Income A/C

Credit

Credit the increase in income

As per accrual-based accounting income must be recognized during the period it is earned irrespective of when the money is received.

Accrued income is also known as income receivable, income accrued but not due, outstanding income and income earned but not received.

Question – On December 31st 2019 Company-A calculated 50,000 as rent earned but not received for 12 months from Jan’19 to Dec’19.

The same is received in cash next year on January 10th 2020. Show all related rent entries including the journal entry for accrued income on these dates;

December 31st 2019 (Same day)

January 10th 2020 (When the payment is received)

1. December 31st 2019 – (Rent earned but not received)

Accrued Rent Account

50,000

To Rent Account

50,000

2. January 10th 2020 – (Received cash in lieu of accrued rent from 2019)

Cash Account

50,000

To Accrued Rent Account

50,000

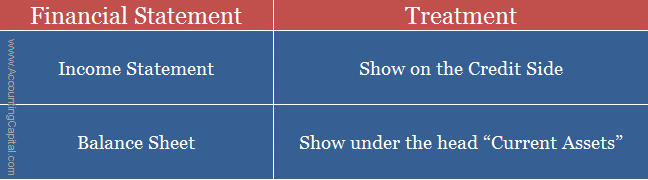

Treatment of Accrued Income in Financial Statements

After posting the journal entry for accrued income a business records it in the final accounts as follows;

Shows it on the asset side of the balance sheet under the head “Current Assets”.

Treatment of accrued income in the books of finance

Example – Journal Entry for Accrued Commission

Let’s assume that in March there was 30,000 as commission earned but not received due to business reasons.

At the end of the month, the company will record the situation into their books with the below journal entry.

Accrued Commission A/C

30,000

To Commission Received A/C

30,000

(Commission earned but not received)

Example – Journal Entry for Accrued Interest

Total of 2000 was not received as interest earned on debentures in the current accounting year. Post the journal entry for accrued income (interest earned) to include the impact of this activity.

Accrued Interest A/C

2,000

To Interest Received A/C

2,000

(Interest receivable on debentures)

Short Quiz for Self-Evaluation

Loading

Your quiz has been submitted

Want to re-attempt? - “Refresh” this page.

Check out more content on our site :)

Subscribed? - Check your mailbox

Thank You!

Server Side Error

We faced problems while connecting to the server or receiving data from the server. Please wait for a few seconds and try again.

If the problem persists, then check your internet connectivity. If all other sites open fine, then please contact the administrator of this website with the following information.

Prepaid expenses are those expenses which are paid in advance for a benefit yet to be received. The perks of such expenses are yet to be utilised in a future period. Below is the journal entry for prepaid expenses;

It involves two accounts: Prepaid Expense Account and the related Expense Account.

They are an advance payment for the business and therefore treated as an asset. The accounting rule applied is to debit the increase in assets” and “credit the decrease in expense” (modern rules of accounting).

They are also known as unexpired expenses or expenses paid in advance. It is important to show prepaid expenses journal entry in the financial statements to avoid understatement of earnings.

Simplifying Prepaid Expenses Adjustment Entry with an Example

Question – On December 20th 2019 Company-A pays 1,20,000 (10,000 x 12 months) as rent in cash for next year i.e. for the period (Jan’2020 to Dec’2020).

Show all entries including the journal entry for prepaid expenses on these dates;

December 20th 2019 (Same day)

December 31st 2019 (End of period adjustment)

January 1st 2020 to December 1st 2020 (Beginning of each month next year)

1. December 20th 2019 – (Payment made for rent due next year)

Rent Account

1,20,000

To Cash Account

1,20,000

2. December 31st 2019 – (Rent payable in next year transferred to prepaid rent account)

Prepaid Rent Account

1,20,000

To Rent Account

1,20,000

3. January 1st 2020 to December 1st 2020 – (Expense charged to each period)

Rent Account

10,000

To Prepaid Rent Account

10,000

All 12 months from Jan’20 to Dec’20 will be charged in each period against the prepaid expense account to reduce the prepaid account to zero by end of the year.

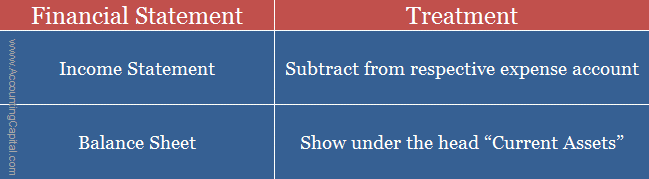

Treatment of Prepaid Expenses in Financial Statements

Once the journal entry for prepaid expenses has been posted they are then arranged appropriately in the final accounts.

Company-A paid 10,000 as insurance premium in the month of December, the insurance premium belongs to the following calendar year hence it doesn’t become due until January of the next year.

At the end of December the company will record this into their journal book using the below journal entry for prepaid expenses;

Prepaid Insurance Premium A/C

10,000

To Insurance Premium A/C

10,000

(Insurance premium related to next year transferred to prepaid insurance premium account)

Example – Journal Entry for Prepaid Salary or Wages

Journalize the prepaid items in the books of Unreal Corp. using the below trial balance and additional information provided along with it.

Prepaid Salaries – 25,000

Prepaid Wages – 10,000

Account

Dr.

Cr.

Salaries

50,000

Wages

20,000

Journal entry for prepaid expenses in the books of Unreal Corp.

Prepaid Salary A/C

25,000

To Salary A/C

25,000

(Salaries related to next year transferred to prepaid salary account)

Prepaid Wages A/C

10,000

To Wages A/C

10,000

(Wages related to next year transferred to prepaid wages account)

Example – Journal Entry for Prepaid Rent

Company-B paid 60,000 rent (5,000 x 12 months) in the month of December which belongs to the next year and doesn’t become due until January of the following year.

Using the concept of the journal entry for prepaid expenses below is the journal entry for this transaction in the books of Company-B at the end of December.

Prepaid Rent A/C

60,000

To Rent A/C

60,000

(Rent related to next year transferred to prepaid rent account)

Short Quiz for Self-Evaluation

Loading

Your quiz has been submitted

Want to re-attempt? - Simply “refresh” this page.

Please check out more content on our site :)

Subscribed? - Check your mailbox

Thank You!

Server Side Error

We faced problems while connecting to the server or receiving data from the server. Please wait for a few seconds and try again.

If the problem persists, then check your internet connectivity. If all other sites open fine, then please contact the administrator of this website with the following information.

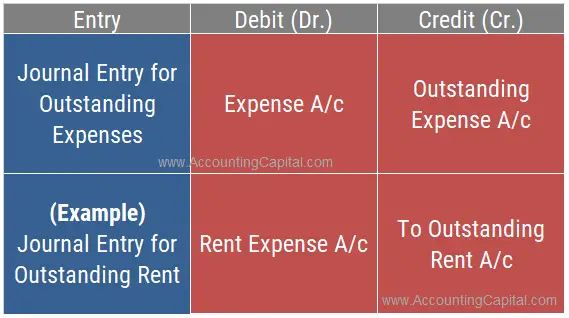

There are expenses that are due but have not been paid as of the end of the current accounting period. Such expenses are called outstanding expenses. The benefits of such expenses have been consumed although due to some reason they are not paid. We’ll explain how to pass a journal entry for outstanding expenses in this article.

Outstanding expense is a “personal” account as per the traditional classification of accounts and a “liability” as per the more recent way of accounting.

Journal Entry for Outstanding Expenses

Expense A/C

Debit

Debit the increase in expense

To Outstanding Expense A/C

Credit

Credit the increase in liability

The outstanding expenses journal entry involves two accounts: the “Outstanding Expense Account” and the related “Expense Account”.

They are an obligation for the business and therefore treated as a liability. The accounting rule applied is “credit the increase in liability” and “debit the increase in expense” (modern rules of accounting).

They are also known as expenses due but not paid and should be shown in the financial books to avoid overstatement of earnings.

Simplifying Outstanding Expenses Entry with an Example

Question – On December 31st 20YY Company-A recognised rent due for 100,000 related to the same year. The period has ended and the payment has not been made.

The same is paid in cash next year on January 10th. Show all financial recordings including the journal entry for outstanding expenses on these dates;

December 31st 20YY (Same day)

January 10th (Next year, when it is actually paid)

1. December 31st 20YY – (Overdue expense recorded as outstanding)

Rent Expense A/c

100,000

To Outstanding Rent A/c

100,000

2. January 10th – (Payment made towards outstanding rent in next year)

Outstanding Rent A/c

100,000

To Cash A/c

100,000

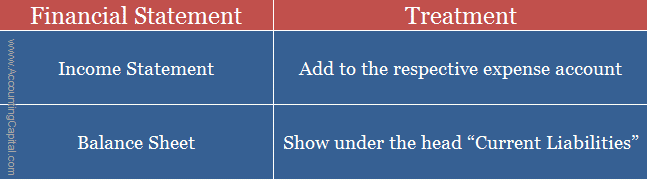

Treatment of Oustanding Expenses in Financial Statements

Once the journal entry for outstanding expenses has been posted they are then placed appropriately in the final accounts.

Salaries and wages differ slightly. Part-time jobs, assignments with variable hours, and jobs with repetitive duties are commonly referred to as wages instead of salaries.

Wages are generally paid on a weekly, biweekly, or monthly basis. Generally, the difference between salary and wage is that salary is a fixed amount and wage is based on the number of hours that an employee works.

Pass outstanding salary journal entry in the books of Unreal Corp. using the below trial balance and supplementary information provided along with it.

Outstanding Salaries – 30,000

Outstanding Wages – 20,000

Extract from Trial Balance of Unreal Corp.

Account

Dr.

Cr.

Salaries

70,000

Wages

80,000

Outstanding Salaries Journal Entry in the Books of Unreal Corp.

Salary A/c

30,000

To Outstanding Salary A/c

30,000

(Salaries due in the previous year are transferred to “Outstanding Salary A/c”)

Journal Entry for Outstanding Wages in the Books of Unreal Corp.

Wages A/c

20,000

To Outstanding Wages A/c

20,000

(Wages related to the previous year transferred to outstanding wages account)

It is also known as accrued interest. An outstanding interest journal entry is required to record the amount of interest owed by the business on a loan obligation. It refers only to the portion of the interest that is currently due but not paid by the borrower. It is a “receivable” for the lender.

Suppose in the month of December, interest on a bank loan taken from ABC bank was due at 24,000. Pass the accounting entry for outstanding interest at the end of the year i.e. 31st Dec.

Outstanding expenses are obligations yet to be paid by the firm. They are “credited” as per two rules of accounting,

Personal A/c – Cr. the giver

Treated as a Liability – Cr. the increase in liability

Such past due expense is debited to Profit & Loss A/c because it is prepared as per the accrual basis of accounting which says that “irrespective of when the payment is made, all expenses and incomes should be recorded in the period when they occurred.

An outstanding expense is one that has been incurred but has not yet been paid. Despite the fact that it has not been paid, it belongs to the same accounting period. Therefore, it is added to the debit side of a profit & loss account.

Debt is typically in the form of money, that is due or owed. However, in day-to-day accounting vocabulary, a “debt” may be referred to as long-term debt i.e. an obligation that is payable beyond 12 months.

Outstanding expenses are a liability for the firm but they are not considered a debt for the company. Due to the fact that outstanding expenses are expected to be paid within 12 months, they are treated as current liabilities.

We faced problems while connecting to the server or receiving data from the server. Please wait for a few seconds and try again.

If the problem persists, then check your internet connectivity. If all other sites open fine, then please contact the administrator of this website with the following information.