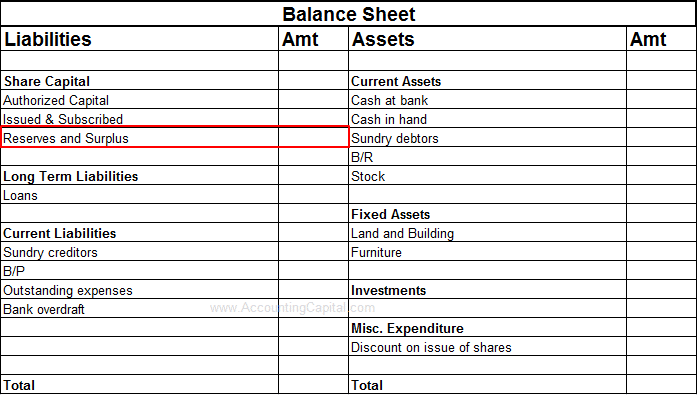

Total cumulative depreciation of a tangible asset up to a specific date is called Accumulated Depreciation. It is the total depreciation already charged as expense in different accounting periods. It is a contra-asset account which, unlike an asset account, has a credit balance.

It is shown on the balance sheet as a deduction from gross fixed assets.

Original Cost of Asset – Accumulated Depreciation = Net Cost (or) Carrying Value (or) Book Value

Example

Let’s assume that a company buys a vehicle for 50,000 with a lifespan of 5 years and no scrap value. According to the straight line method of depreciation, the asset will be depreciating at 10,000/year.

Accumulated Depreciation

Carrying Value

Year 1

10,000

50,000 – 10,000 = 40,000

Year 2

10,000 x 2

40,000 – 10,000 = 30,000

Year 3

10,000 x 3

30,000 – 10,000 = 20,000

Year 4

10,000 x 4

20,000 – 10,000 = 10,000

Year 5

10,000 x 5

10,000 – 10,000 = 0

The purpose of a contra-asset account such as this is to reduce the book value of an asset to show the loss of value due to wear and tear.

Companies buy assets such as buildings, furniture, machinery, etc., all of which lose their value with everyday use. This depreciation loss is to be accounted for in the books of accounts to show the most accurate picture of the financial statements of a business.

Journal Entries related to Accumulated Depreciation

In the above table, the journal entries would be:

Journal entry to be done annually to show the accumulated depreciation.

Depreciation A/C

10,000

To Accumulated Depreciation A/C

10,000

After 5 years the machine’s scrap value is zero. To remove both the vehicle and its related depreciation from the company’s accounting records.

Accumulated Depreciation A/C

50,000

To Vehicle A/C

50,000

Short Quiz for Self-Evaluation

Loading

Your quiz has been submitted

Want to re-attempt? - “Refresh” this page.

Check out more content on our site :)

Subscribed? - Check your mailbox

Thank You!

Server Side Error

We faced problems while connecting to the server or receiving data from the server. Please wait for a few seconds and try again.

If the problem persists, then check your internet connectivity. If all other sites open fine, then please contact the administrator of this website with the following information.

An honorarium is a voluntary payment given to a person for services delivered. These are generally acts or services for which customs and traditions disallow a price to be set. Payments are made just as a gesture to thank or appreciate the person for rendering the services. The honorarium is not legally required.

Example

A person was told to judge a competition for which the sponsors were only willing to offer an honorarium, so, legally there is no payment to be made for this task. There is no salary, it is not a freelance or an hourly contract.

Another example of an honorarium could be a situation where a person gives a speech at a conference, he/she may receive an honorarium for the service.

In accounting, Grouping refers to presenting similar items with similar qualities together. They are shown under a common head inside financial statements. For example, let’s say a company has 200 different creditors that it deals with. All of them will not be shown separately in financial statements, only the net total of all the creditors will be presented.

Another example would be of Stock which shows the net total of (Raw Material + Work In Progress + Finished Stock).

The arrangement of assets and liabilities on the balance sheet in proper order is called Marshalling. The assets, liabilities, and capital on a balance sheet must be properly marshalled and shown in a logical order. There are 2 common ways of Marshalling:

By Liquidity

Assets are arranged in order of liquidity i.e. they can be converted to cash easily. Most liquid assets, such as cash, will come first and least liquid assets, such as building, will come last. Liabilities are arranged in the order they are to be discharged.

Sample Format of a Balance Sheet in Order of Liquidity

Liabilities

Amt

Assets

Amt

Bills Payable

xxxx

Cash

xxxx

Creditors

xxxx

Bank

xxxx

Loans

xxxx

Govt. Securities

xxxx

Outstanding Expenses

xxxx

Other Investments

xxxx

Reserves & Surplus

xxxx

Bills Receivable

xxxx

Capital

xxxx

Debtors

xxxx

Stock

xxxx

Furniture

xxxx

Plant & Machinery

xxxx

Building

xxxx

By Permanence

Assets are arranged in order of permanency i.e. with the most permanent on the top and the most liquid on the bottom. Liabilities which have to be discharged last are shown first and those which have to be discharged first are shown last.

Sample Format of a Balance Sheet in Order of Permanence

Liabilities

Amt

Assets

Amt

Capital

xxxx

Building

xxxx

Reserves & Surplus

xxxx

Plant & Machinery

xxxx

Outstanding Expenses

xxxx

Furniture

xxxx

Loans

xxxx

Stock

xxxx

Creditors

xxxx

Debtors

xxxx

Bills Payable

xxxx

Bills Receivable

xxxx

Other Investments

xxxx

Govt. Securities

xxxx

Bank

xxxx

Cash

xxxx

Short Quiz for Self-Evaluation

Loading

Your quiz has been submitted

Want to re-attempt? - “Refresh” this page.

Check out more content on our site :)

Subscribed? - Check your mailbox

Thank You!

Server Side Error

We faced problems while connecting to the server or receiving data from the server. Please wait for a few seconds and try again.

If the problem persists, then check your internet connectivity. If all other sites open fine, then please contact the administrator of this website with the following information.

As the name suggests, accounting techniques that are used during the times of high inflation are called Inflation Accounting. It is widely used to counter the effect of historical cost accounting at the times of high inflation. It is also called price Level Accounting.

Inflation has an effect on prices, but corporate finances also become vulnerable due to the rise in prices and financial statements may not show the true value. Adjustments are made to rectify this so the financial statements show a true picture of business.

In developed nations, the inflation rate is generally stabilized. Developing and under-developed nations would generally have a high rate of inflation. Therefore, in the 2nd case, examining the books of accounts is difficult, because historical information is less convincing and relevant as prices increase rapidly.

Short Quiz for Self-Evaluation

Loading

Your quiz has been submitted

Want to re-attempt? - “Refresh” this page.

Check out more content on our site :)

Subscribed? - Check your mailbox

Thank You!

Server Side Error

We faced problems while connecting to the server or receiving data from the server. Please wait for a few seconds and try again.

If the problem persists, then check your internet connectivity. If all other sites open fine, then please contact the administrator of this website with the following information.

The Cost of Goods, also known as COGS or Cost of Sales, is the actual cost of the commodities sold to customers. It involves both costs of the material used for production and direct labour cost. The cost of goods sold (COGS) is shown in the income statement. Sales are either recorded in a company’s cash book or the sales book.

It includes;

Raw material, Storage, Freight or Shipping Charges

Factory Overheads

Direct Labor Cost

How to Calculate the Cost of Goods Sold (COGS)?

COGS = Opening Stock + Purchases – Closing Stock

Also, COGS = Net Sales – Gross Profit

Example 1

Opening Stock of a business is valued at = 2,500,000

Purchases = 1,000,000, Closing Stock valued at = 1,500,000

COGS = OS + P – CS

= 2,500,000 + 1,000,000 – 1,500,000

= 2,000,0000

Example 2

Net Sales = 2,000,000, Gross Profit = 1,000,000

COGS = Net Sales – GP

= 2,000,000 – 1,000,000

= 1,000,000

Short Quiz for Self-Evaluation

Loading

Your quiz has been submitted

Want to re-attempt? - “Refresh” this page.

Check out more content on our site :)

Subscribed? - Check your mailbox

Thank You!

Server Side Error

We faced problems while connecting to the server or receiving data from the server. Please wait for a few seconds and try again.

If the problem persists, then check your internet connectivity. If all other sites open fine, then please contact the administrator of this website with the following information.

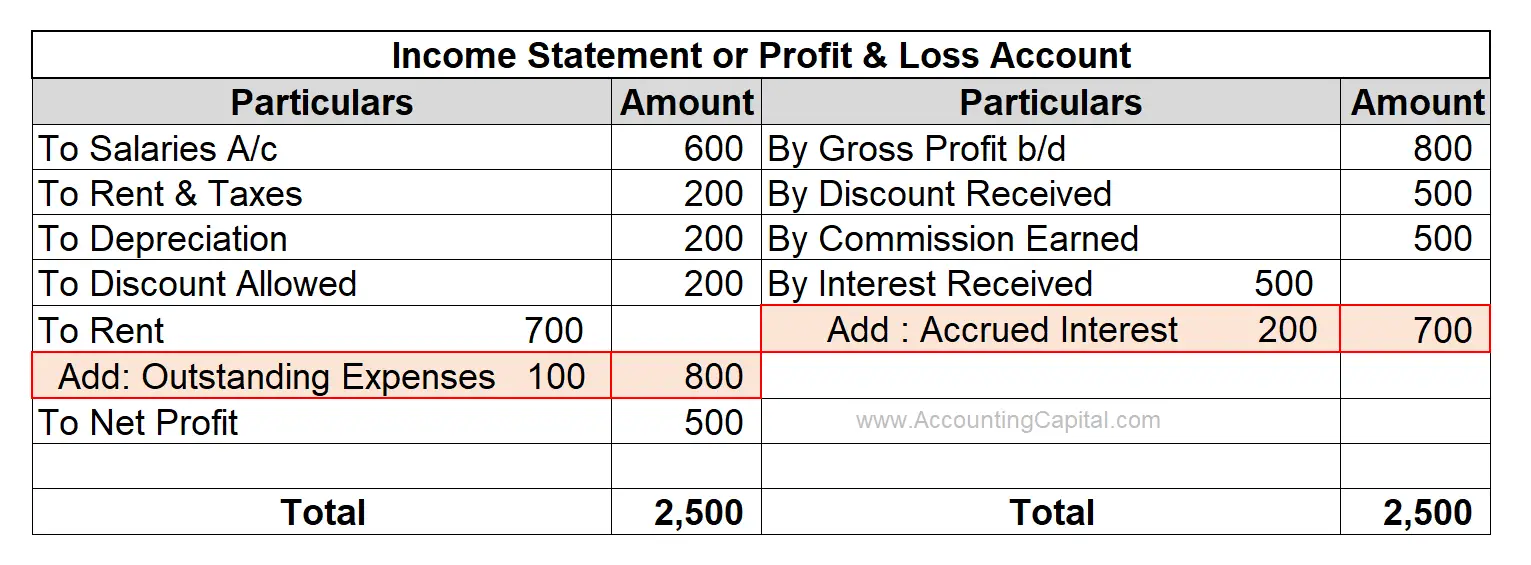

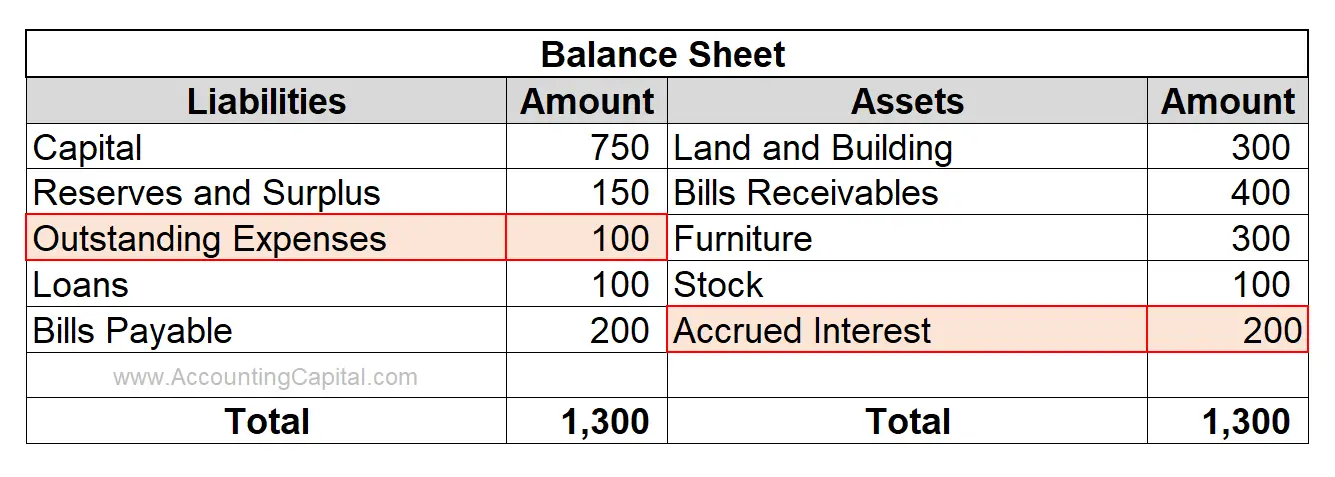

To understand Accruals we need to understand the meaning of the word accrual, which is “The act of accumulating something”. Accruals are mainly related to prepayments and arrears.

In accrual-based accounting, accruals refer to expenses and revenues that have been incurred or earned but have not been recorded in the books of accounts. Adjustment entries are incorporated in the financial statements to report these at the end of an accounting period.

In other words, they consist of balance sheet accounts that are a liability or non-cash based assets. A few examples of accruals may include accounts receivables, accounts payable, accrued rent, etc.

Accrued Expense is an expense which has been incurred, but has not been recorded in the books of accounts presently. It will require an adjustment entry in the books of accounts to reflect this in the financial statements.

Accrued Income is an income which has been earned, but has not been recorded in the books of accounts presently. Similar to accrued expenses, an adjustment entry will be required in this case too.

Money owed by a business in the current accounting period is to be accrued and should be added to the expenses in the profit and loss account.

Money that is owed to a business in the current accounting period is to be accrued and should be added to the income in the profit and loss account.

Examples of Accruals

Illustration 1

A company pays 25,000 to rent every month. On January, 1 it decides to pay 1,00,000 advance towards rent.

Accruals related treatment – The company will not record the payment as an expense immediately because the building has not been used yet. So when they report their quarterly results after March, 31, they will report expenses for 3 months i.e. 25,000 x 3 months = 75,000 because the building will only be used for 3 months till that time.

Illustration 2

Another example is when a company is supposed to receive 25,000 per month as rent but the tenant pays 1,00,000 on January, 1 in advance.

Accruals related treatment – The company will not record the received amount as income till the building has been used. So, again during the quarterly results after March, 31, they will report income for 3 months i.e. 25,000 x 3 months = 75,000 because the building will only be used for 3 months until that time.

Where Should Accruals be Recorded?

Short Quiz for Self-Evaluation

Loading

Your quiz has been submitted

Want to re-attempt? - “Refresh” this page.

Check out more content on our site :)

Subscribed? - Check your mailbox

Thank You!

Server Side Error

We faced problems while connecting to the server or receiving data from the server. Please wait for a few seconds and try again.

If the problem persists, then check your internet connectivity. If all other sites open fine, then please contact the administrator of this website with the following information.

Contra account is an account which is used to reduce or offset the value of an associated account. It holds opposite sign for a particular type of account.

If an account has debit balance (e.g for an Asset a/c), then there will be a credit balance in its contra account. The opposite is true for a liability account.

It is shown on a company’s balance sheet. It can be used for any type of account such as asset, liability, capital, revenue.

Examples of Contra Account

Drawings Account

Account

Balance

Capital Account

Credit

Drawings Account (Contra)

Debit

An example where drawings account is a contra a/c linked to company’s capital account.

Account

Balance

Capital Account

2,00,000

Drawings Account

(50,000)

Net Capital

2,00,000 + (50,000) = 1,50,000

Plant and Machinery Account

Account

Balance

Asset Account

Debit

Accumulated Depreciation Account (Contra)

Credit

An example where accumulated depreciation account of plant and machinery is a contra a/c account linked to company’s plant and machinery.

Account

Balance

Plant and Machinery Account

5,00,000

Accumulated Depreciation Account

(60,000)

Book Value of Plant and Machinery

5,00,000 + (60,000) = 4,40,000

Uses of Contra Account

It is used to offset another account, for instance, debtors have a debit balance of 50,000 however the associated contra account i.e. “provision for doubtful debts” has a credit balance of 10,000. The net numbers for debtors would be (50k-10k) = 40,000.

It is also used to correct errors made with an account.

It helps to make financial records transparent. Simply looking at the accounting records of a given business, one can reach back to the history related to certain debits and credits.

Also known as COA, chart of accounts is a list of all accounts in a company’s general ledger. They are the identified accounts which are available for a company to record transactions.

ERPs such as Oracle, SAP, etc., can allow each account a unique number as defined. With this, it can be identified and modified according to the business’ needs.

Think of chart of accounts as a Tree!

“Assets” will be branches of the tree.

“Current assets, fixed assets, other assets” are its sub-branches.

Finally, accounts such as Cash, Bank, Debtor, Prepaid Insurance are like leaves of the sub-branches.

Keeping the same fundamentals, chart of accounts tree can be differently designed for separate businesses depending on need, size and divisions inside a company.

Below is a sample listing of the order where accounts appear inside chart of accounts.

Type of Accounts

Sub Classification Examples

Balance Sheet Accounts

Assets

E.g. Current Assets, Fixed Assets, Other Assets

Liabilities

E.g. Current Liabilities, Long-Term Liabilities

Capital

E.g. Equity

Profit & Loss Accounts

Operating Revenues & Gains

E.g. Sales

Non-Operating Revenues & Gains

E.g. Profit on sale of assets

Operating Expenses

E.g. Cost of goods sold

Non-Operating Expenses & Losses

E.g. Loss on sale of assets

Few reasons for using the chart of accounts

Chart of accounts helps in differentiating and properly recording different types of transactions such as Assets, Liabilities, Capital, Revenue, Expenditure, etc.

Chart of accounts also helps in efficiently organizing and managing the financial data.

Just like the above accounts, chart of accounts will have different groups such as capital, revenue and expenditure with their subtypes, accounts and individual account numbers to record transactions.

Short Quiz for Self-Evaluation

Loading

Your quiz has been submitted

Want to re-attempt? - “Refresh” this page.

Check out more content on our site :)

Subscribed? - Check your mailbox

Thank You!

Server Side Error

We faced problems while connecting to the server or receiving data from the server. Please wait for a few seconds and try again.

If the problem persists, then check your internet connectivity. If all other sites open fine, then please contact the administrator of this website with the following information.

The word reconcile means “making one thing consistent with another”.In case of business, a Bank Reconciliation Statement or BRS refers to a statement which is made to reconcile bank balance shown on the bank statement or passbook with the bank balance shown in the cash book.This helps a business to keep control of cash and get satisfactory explanations regarding differences between both balances.

These days cash book balances are generally extracted from the company’s accounting ERP and the bank statements are obtained from daily bankfeeds. The reconciliation is either done manually with the help of MS-Excel or is partly automated with help of a few additional software packages.

Both the internal source (cash book) and the external source (a bank statement or a passbook) are reconciled with each other, then all the mismatches are identified and properly recorded.

Two Things to Remember are

Bank Reconciliation Statement should be prepared when a bank statement is received or a passbook is updated.

BRS is made and shown for a specific date.

Why Do We Prepare a Bank Reconciliation Statement (BRS)?

The differences in the two balances arise due to 3 main reasons: Timing, Errors, and Transactions only known to the bank. Overall, the main reason for preparing BRS is to have a strict internal control over company’s cash inflows and outflows. To be more precise, these are a few reasons why we prepare BRS.

S.No.

Scope

Comments

1.

Mistakes and Errors

Bank reconciliation statement helps to detect any errors and mistakes in cash or a passbook.

2.

Explains Delay

Any delay in clearance or collection of checks can be identified.

3.

Fraud Detection

Timely reconciliations help prevent and find any frauds related to cash.

4.

Actual Bank Balance

It helps to identify the actual bank balance of a business.

5.

Valid Transactions

It helps in separating valid and invalid transactions such as a wrongly charged fee by the bank.

Short Quiz for Self-Evaluation

Loading

Your quiz has been submitted

Want to re-attempt? - “Refresh” this page.

Check out more content on our site :)

Subscribed? - Check your mailbox

Thank You!

Server Side Error

We faced problems while connecting to the server or receiving data from the server. Please wait for a few seconds and try again.

If the problem persists, then check your internet connectivity. If all other sites open fine, then please contact the administrator of this website with the following information.

Expenses are costs incurred for a consideration. An expense may be capital or revenue in nature and usually incurred by disbursal of money. Capex and Opex refer to capital expenditure and operating expenditure respectively.

They can also be recognized by agreeing to pay off an obligation e.g. paying rent, buying machinery, paying taxes, etc.

Capital Expenditure (Capex)

Also known as Capex it is an expenditure incurred by a business to acquire fixed assets or add value to them in view of creating future benefits. The benefits derived from capital expenditure extend beyond the accounting period of the actual spend. The assets acquired in question might be tangible or intangible.

This will include everything from costs incurred for installation of a fixed asset, legal costs to acquire it, extension or improvement of fixed assets.

This type of expenditure is shown in the balance sheet on the asset side.

All these are examples of Capex (Capital Expenses) incurred by a business. Even the upgrading and installation cost will qualify as a capital expenditure.

Also known as operational expenditure and operating expense, it is an ongoing cost that a business has to spend to run its day-to-day operations. The benefits derived from such expenses are exhausted within the same accounting period and don’t carry forward. It is the opposite of capital expenditure.

This type of expenditure is shown in the income statement on the debit side.

Examples of Operating Expenditure (Opex)

Telephone, Electricity, Maintenance and Repairs, Carriage are few examples of Opex (Operating Expenses)

Short Quiz for Self-Evaluation

Loading

Your quiz has been submitted

Want to re-attempt? - Simply “refresh” this page.

Please check out more content on our site :)

Subscribed? - Check your mailbox

Thank You!

Server Side Error

We faced problems while connecting to the server or receiving data from the server. Please wait for a few seconds and try again.

If the problem persists, then check your internet connectivity. If all other sites open fine, then please contact the administrator of this website with the following information.

Accounting involves the creation, management, summation & communication of day-to-day transactions of a business ultimately leading to the preparation of financial statements.

On the other hand, finance has a wider scope and is mainly responsible to support in decision-making such as investment, divestment, cash management, Working capital management etc.

Difference between finance and accounting (table format)

Finance

Accounting

1. Finance is a branch of economics which deals with the efficient management of assets and liabilities.

1. Accounting is the occupation of summarizing financial transactions which were classified in the ledger account as a part of book-keeping.

2. It is a pre-mortem study of the organization’s funds or asset requirements.

2. It is a postmortem task of the recording of what has actually happened.

3. The aim of finance includes decision-making, strategy, managing & controlling.

3. The aim of accounting is to collect and present financial information for both internal and external purposes.

4. Determination of funds is based on a cash flow system, actual receipts and payments are recognized for revenue and payments.

4. Determination of funds is based on the accrual system, i.e. revenue is acknowledged at the point of sale and not when it is collected. Expenses are also recognized when they are incurred.

5. Few tools of finance include Ratio analysis, Risk management, Returns on investment, etc.

5. Few tools of accounting include Trading account, P&L account, Balance sheet, Cash flow statement, etc.

Finance and Accounting are both distinct, but complementary to each other.

Short Quiz for Self-Evaluation

Loading

Your quiz has been submitted

Want to re-attempt? - Simply “refresh” this page.

Please check out more content on our site :)

Subscribed? - Check your mailbox

Thank You!

Server Side Error

We faced problems while connecting to the server or receiving data from the server. Please wait for a few seconds and try again.

If the problem persists, then check your internet connectivity. If all other sites open fine, then please contact the administrator of this website with the following information.

In the dual entry accounting system, a contra entry is an entry which is recorded to reverse or offset an entry on the other side of an account. If a debit entry is recorded in an account, it will be recorded on the credit side and vice-versa.

Debit and credit aspects of a single transaction are entered in the same account but in different columns. Each entry, in this case, is viewed as a contra entry of the other. Remember the word contra as “Against” or “Opposite”.

Examples of Contra Entry

1. Cash 50,000 withdrawn for an official purpose from the bank. Journal entry for this transaction will be

Cash A/C

50,000

To Bank A/C

50,000

In the above example, both entries, debit, and credit, are a contra entry of each other, they both offset each other. The narration is not required for such an entry and only a “C” is written in the left column which depicts that it is a contra entry.

2. Cash 10,000 received from a debtor is deposited into the bank

Bank A/C

10,000

To Cash A/C

10,000

The above amount is recorded in the bank column (debit) side of the double column cash book.

A contra entry is also used in the Intercompany netting to offset receivables and payables between 2 different legal entities/subsidiaries of a company so that one final (net) amount remains.

It will be easier to understand the meaning of deferred revenue expenditure if you know the word deferred, which means “Holding something back for a later time”, or “postpone”.

Deferred Revenue Expenditure is an expenditure that is revenue in nature and incurred during an accounting period, however, related benefits are to be derived in multiple future accounting periods.

These expenses are unusually large in amount and, essentially, the benefits are not consumed within the same accounting period.

Part of the amount which is charged to the profit and loss account in the current accounting period is reduced from total expenditure and the rest is shown in the balance sheet as an asset (fictitious asset, i.e. it is not really an asset).

Suppose that a company is introducing a new product to the market and decides to spend a large amount on its advertising in the current accounting period. This marketing spend is supposed to draw benefits beyond the current accounting period.

It is a better idea not to charge the entire amount in the current year’s P&L Account and amortize it over multiple periods.

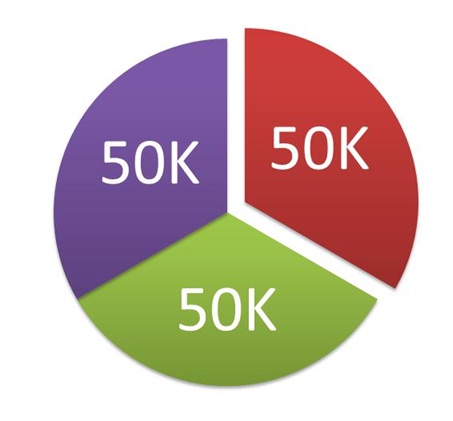

The image shows a company spending 150K on advertising, which is unusually large as compared to the size of their business.

The company decides to divide the expense over 3 yearly payments of 50K each as the benefits from the spending are expected to be derived for 3 years.

50K will be shown in the current P&L and the remaining Amt. in BS

*Large losses originating from unforeseen circumstances, such as a natural disaster or fire, etc., may also be treated as deferred revenue expenditure.

Reasons

The benefits of such an expense are to be received in the future financial years. Therefore, it is logically incorrect to record 100% of such expenses as revenue expenditures and write them off in the current accounting period.

In most cases, these expenses are so large that they may consume all the profits of the company if written off in the current accounting year. As a result, the users of accounting information will get a false impression.

Short Quiz for Self-Evaluation

Loading

Your quiz has been submitted

Want to re-attempt? - Simply “refresh” this page.

Please check out more content on our site :)

Subscribed? - Check your mailbox

Thank You!

Server Side Error

We faced problems while connecting to the server or receiving data from the server. Please wait for a few seconds and try again.

If the problem persists, then check your internet connectivity. If all other sites open fine, then please contact the administrator of this website with the following information.

TextStatus: undefined HTTP Error: undefined

Processing you request

Error

Some error has occured.

Revision & Highlights Short Video

Highly Recommended!!

Do not miss our 1-minute revision video. This will help you quickly revise and memorize the topic forever. Try it :)

The word contingent or contingency means “possible, but not certain to occur”. So, according to the definition, contingent liabilities are those liabilities that may or may not be incurred by a business depending on the outcome of a future event. The existence of this kind of liability is completely dependent on the occurrence of a probable event in future.

An example of such liability is a court case, only if the company loses the court case, contingent liability will actually be realized. In another example of contingent liabilities acting as a surety/guarantor on a loan and assuming the responsibility of paying it back in case of default may also be a case of contingent liability since if the principal debtor fails to pay you will be required to reimburse.

Unlike contingent assets, contingent liabilities are required to be disclosed as soon as they can be estimated, usually as a footnote to the balance sheet. If the possibility of the outflow of money or assets is remote then the disclosure may not be necessary.

There are two questions that need to be answered if a contingent liability is to be recorded with a journal entry:

Is the contingent liability probable?

Can the amount of obligation be estimated?

Example

Patent wars that usually happen between Top brands give a clear-cut explanation. Let’s suppose that Apple files a case of a patent violation on Samsung and Samsung not only realizes that it may have to pay for violations but also estimates how much in total. In this case, Samsung will record the estimated amount in their books of accounts as a Contingent Liability.

Short Quiz for Self-Evaluation

Loading

Your quiz has been submitted

Want to re-attempt? - Simply “refresh” this page.

Please check out more content on our site :)

Subscribed? - Check your mailbox

Thank You!

Server Side Error

We faced problems while connecting to the server or receiving data from the server. Please wait for a few seconds and try again.

If the problem persists, then check your internet connectivity. If all other sites open fine, then please contact the administrator of this website with the following information.

Reserves and provisions are somewhat alike but are created for different reasons and under distinct circumstances. Both are important for a business and one can’t reduce the importance of the other. This article covers major points of difference between reserves and provisions.

Reserves are what a business would put away from its profits for future contingencies and strengthening of the business, whereas, provisions are aimed to satisfy an anticipated known expenditure.

Reserves

Provisions

1. Reserves are made to strengthen the financial position of a business and meet unknown liabilities & losses.

1. Provisions are made to meet specific liability or contingency, e.g. a provision for doubtful debts.

2. Reserves are only made when the business is profitable.

2. Provisions are made irrespective of profits earned or losses incurred by a business.

3. They can be used to distribute dividends to shareholders.

3. They cannot be used to distribute dividends as they are made for a specific liability.

4. They are made by debiting P&L Appropriation Account.

4. They are made by debiting the P&L Account.

5. It is not mandatory to create reserves for the business, it is mainly done for prudence.

5. It is mandatory to create provisions as per various laws.

6. Reserves are shown on the liability side of a balance sheet.

6. Provisions are either shown on the liability side of a balance sheet or as a deduction from the concerned asset.

7. It may be used for investment outside the business.

7. It can not be used for investment purposes.

Reserves

They are the portion of profits set aside to strengthen the financial position of a business. Generally, reserves are created to meet unknown future obligations which may arise due to miscellaneous business reasons.

For example – General reserve, reserve for expansion, dividend equalisation reserve, debenture redemption reserve, capital redemption reserve, increased replacement cost reserve, etc.

Specific reserves, as the name suggests are made for specific reasons and may only be used for that specific purpose. One major difference between reserves and provisions is that a provision is always specific, however, reserves may be generic.

They are shown in the balance sheet along with share capital.

Provisions

They are the portion of profits set aside to meet known losses/expenses in the future. The main purpose to create provisions is to meet recognized future obligations which may arise due to a specific business reason.

Reserve means the amount set aside out of profits or other surpluses that are not meant to cover any liability, contingency, commitment, or legal requirement. Thus, the reserve covers the case of an amount that is neither a liability nor a provision. The following are the important types of reserves:

Capital Reserve- It is an accounting mechanism for conserving profits. It imparts an element of stability to the overall finances of a business enterprise. Capital reserve arises either as a gain on the sale of long-term assets or a settlement of liabilities. It does not include any free balance that might be used for the distribution of profits. Examples of the capital reserve are:

Profits emerging from the revaluation of fixed assets

Profits accruing on the sale of fixed assets

Profits from the re-issue of shares

Profits prior to incorporation of a company

Revenue Reserves – Revenue reserves are created out of revenue profit that is usually distributable profits. All distributable profits are not always available for paying dividends since a certain amount may be required to be kept aside either by law (minimum) or as a managerial decision (higher amount) for business needs. It is only after this that the profits will be available for distribution. A few examples are:

General Reserve

Dividend Equalization Reserve

Debenture Redemption Reserve

General Reserve – General reserve is a retention of a portion of revenue profits for the improvement of the overall financial status of an enterprise and to improve its health in general. It is a salient feature of corporate finance. The creation and maintenance of a general reserve helps in-

Conserving resources

Saving for unforeseen losses

Scope of business expansion

Specific Reserves – A business undertaking in contemporary times is involved in a range of business activities in pursuance of its goal of creating value in the organization. Some of the contingency situations can be looked after and financially managed by the creation of provisions for known events. Management may like to provide a second line of defence against some of these. A specific reserve is created for such a given purpose. A few examples are:

Contingency reserve

Capital Redemption reserve

Workmen Compensation reserve

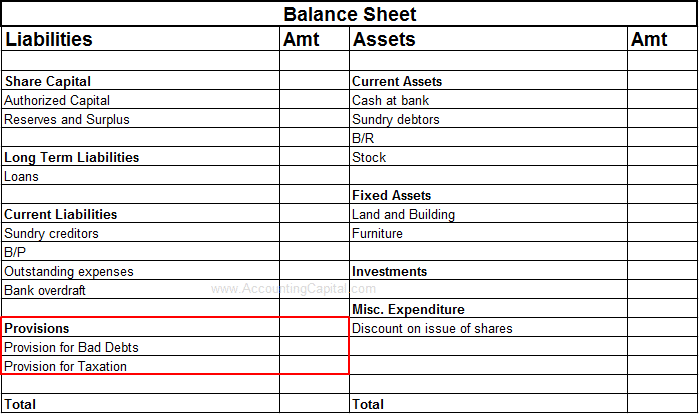

Types of Provisions

The provision means an amount that is written off or retained, kept aside by way of providing for depreciation; or retained by way of providing for any unknown future liability of which the amount can not be ascertained with reasonable accuracy. Important types of Provision are-

Provision for Doubtful Debts – When it is certain that a debt will not be recovered, the amount is written off as bad debt. But, it is also likely that some of the remaining debts may not be recovered in full. This will be a loss to the business.

Hence, it is a common practice to make a suitable provision for doubtful debt at the time of ascertaining profit and loss. Such a provision is made by debiting the number of doubtful debts to the profit and loss account and crediting the account of provision for doubtful debts.

Provision for Discount on Debtors – In practice, business enterprises allow cash discounts to their customers. The tenure of that discount may spill over into the following accounting year for the sales made during the current year.

This requires a provision to be made on debtors and is treated as a loss for the current year. Provision for discount on debtors is created by debiting the profit and loss account and crediting the amount for provisions for a discount on debtors.

Provision for Taxation – A provision for taxation is created and maintained to meet the income tax payable which is a liability for the business, in the current year. Such provision is created by debiting the Income-tax amount of the profit and loss account for that year and crediting the amount for provision for taxation.

Provision for Depreciation – Provision for depreciation is the specific portion of depreciation for that accounting year. Depreciation is by principle charged at the end of the accounting year, and this leads to a lowering of the book value of the asset. However, this reduction isn’t accounted for by crediting the asset account in question, because the assets are going to be continued to be shown on the balance sheet at their original price.

Instead, these depreciation amounts are attributable to a specific account named ‘Accumulated Depreciation‘ which records the collective provisions for depreciation. Such provision is created by debiting the depreciation account and crediting the amount of provision for depreciation.

Reserves Vs Surplus

Following are the differentiating factors between Reserves and Surplus:

Meaning – Reserve is the amount set aside out of undivided profits and other surpluses in order to strengthen the financial position of the business, but not designed to meet any liability or contingency known to exist on the date of the Balance Sheet. The surplus is the credit balance of the profit and loss account after providing for dividends, bonuses, provision for taxation and general reserves, and all other external payments.

Creation – Reserves are an appropriation out of profits and are created only if profit has been earned. It is a matter of financial prudence. What remains after reserves have been created, of the profit earned in that year, is termed as surplus for that accounting period.

Purpose – General Reserves can be used by the company to meet any obligation unknown at that point in time. This includes issuing bonus shares, and dividend equalization, among others. The surplus is the “extra” funds available to the business and shows the operational stability of the company. It is usually transferred to the next year as retained earnings.

Short Quiz for Self-Evaluation

Loading

Your quiz has been submitted

Want to re-attempt? - Simply “refresh” this page.

Please check out more content on our site :)

Subscribed? - Check your mailbox

Thank You!

Server Side Error

We faced problems while connecting to the server or receiving data from the server. Please wait for a few seconds and try again.

If the problem persists, then check your internet connectivity. If all other sites open fine, then please contact the administrator of this website with the following information.

An asset is a useful/valuable thing or person. Assets are divided in various ways depending on their physical existence, life expectancy, nature, etc. The difference between tangible assets and intangible assets is purely based on their physical existence in a business.

In simpler words, an asset is a piece ofproperty owned by an individual or organization which is recognized as having value and is available to meet obligations.

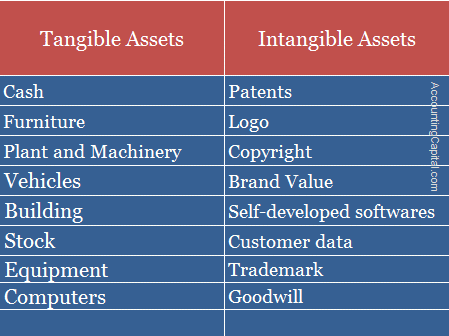

Tangible Assets

The best way to remember tangible assets is to remember the meaning of the word “Tangible” which means something that can be felt with the sense of touch.Assets which have a physical existence and can be touched and felt are called Tangible Assets. The main difference between tangible and intangible assets is where one can be touched and felt the other only exists on paper.

Tangible assets can include both fixed and current assets. A few examples of such assets include furniture, stock, computers, buildings, machines, etc.

Intangible Assets

The opposite of tangible assets, Intangible assets don’t have a physical existence and cannot be touched or felt.Intangible assets can either be definite or indefinite, depending on the kind of asset in question.

A few examples of such assets include goodwill, patent, copyright, trademark, company’s brand name, etc.

A patent is a definite intangible asset as it will expire after the patent is over, however, a company’s brand name will remain over the course of the company’s existence.

Difference between Tangible and Intangible Assets (table format)

Tangible Assets

Intangible Asset

1. They have a physical existence.

1. They don’t have a physical existence.

2. Tangible assets are depreciated

2. Intangible assets are amortized.

3. Are generally much easier to liquidate due to their physical presence.

3. Are not that easy to liquidate and sell in the market.

4. The cost can be easily determined or evaluated.

4. The cost is much harder to determine for Intangible assets.

5. They have a scrap value.

5. They do not have a scrap value.

6. May be accepted by financial institutions as collateral.

6. They are not accepted by financial institutions as collateral.

7. Such assets are held both on paper and by possession.

7. Such assets are held just on paper.

8. Examples: Vehicles, Plant & Machinery, etc.

8. Examples: Software, Logo, Patents, etc.

Short Quiz for Self-Evaluation

Loading

Your quiz has been submitted

Want to re-attempt? - Simply “refresh” this page.

Please check out more content on our site :)

Subscribed? - Check your mailbox

Thank You!

Server Side Error

We faced problems while connecting to the server or receiving data from the server. Please wait for a few seconds and try again.

If the problem persists, then check your internet connectivity. If all other sites open fine, then please contact the administrator of this website with the following information.

TextStatus: undefined HTTP Error: undefined

Processing you request

Error

Some error has occured.

Revision & Highlights Short Video

Highly Recommended!!

Do not miss our 1-minute revision video. This will help you quickly revise and memorize the topic forever. Try it :)

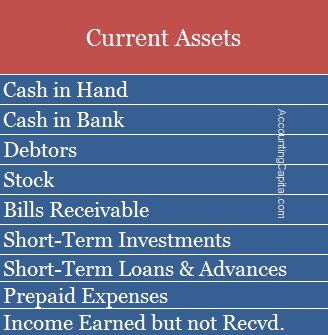

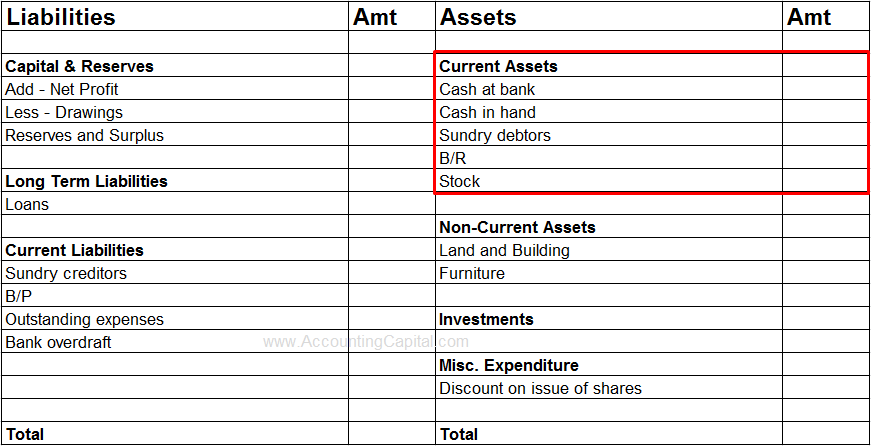

Current assets are assets which are held by a business for a short period, mainly a year, or within an accounting cycle of a business. These are balance sheet accounts which can either be converted to cash or used to pay current liabilities within the same time frame.

These are typically seen as those assets which can easily be converted to cash to pay off current liabilities and outstanding debt payments.

Greater the number higher the liquidity of a company which leads to more working capital. It is important because it is used day in and day out to pay off a firm’s usual expenditure which is important for its operations. Such expenses include utility bills, short-term debts, overheads etc.

Examples of Current Assets

The list of current assets includes Cash, Bank, Debtors, Stock, Prepaid Expenses, etc. They are shown on the Assets side of the balance sheet.

Such short-term assets are also called circulating assets, circulating capital, or floating assets.

They are shown in the assets section of the balance sheet.

The current ratio which can be calculated as CA/CL also highlights the importance of having enough short-term assets vs. short-term liabilities.

It is used to determine the current assets turnover ratio for a company enabling evaluation of how well the company is using them to generate revenue. It can be calculated as (Total Net Sales/Average Current Assets).

Short Quiz for Self-Evaluation

Loading

Your quiz has been submitted

Want to re-attempt? - Simply “refresh” this page.

Please check out more content on our site :)

Subscribed? - Check your mailbox

Thank You!

Server Side Error

We faced problems while connecting to the server or receiving data from the server. Please wait for a few seconds and try again.

If the problem persists, then check your internet connectivity. If all other sites open fine, then please contact the administrator of this website with the following information.

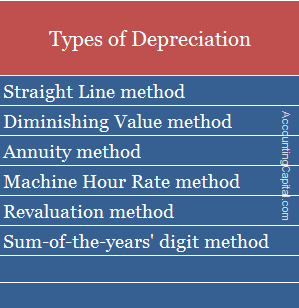

Depreciation is a reduction in the value of a tangible fixed asset due to normal usage, wear and tear, new technology, or unfavourable market conditions. Unlike amortization, which is applied to intangible assets, depreciation is applicable to tangible assets.

In Simple Terms – Depreciation is when an asset loses value over time. This can be due to normal wear & tear, outdated technology, etc. Imagine you have a mobile phone that costs 5,000 & has a life of two years. It means 2,500 worth of value will disappear per year due to day-to-day usage (50%). This is the depreciation percentage & 2,500 is the depreciation amount.

Assets such as plant and machinery, furniture, building, vehicle, etc. which are expected to last more than one year, but not for infinity, are subject to such reduction. It is an allocation of the cost of a fixed asset in each accounting period during its expected time of use.

First, among types of depreciation methods is the straight-line method, also known as the Original cost method, Fixed instalment method, and Fixed percentage method.

The simplest & most used method of charging such a reduction is the straight-line method. An equal amount is allocated in each accounting period.

The rate of reduction is the reciprocal of the estimated useful life of an asset, so, for example, if the useful life of an asset is 5 years, the percentage charged will be 1/5 = 20%.

According to the Straight Line Method,

Depreciation Amt = (Cost of an asset − Salvage Value) / Useful life of the asset in years

Example – Straight Line Method

Asset cost = 1,000,000

Depreciation Rate = 20%

1st year = 20/100*1,000,000

=>2,00,000

2nd year = 20/100*1,00,000

=>2,00,000

Advantages of Straight Line Method are;

Simple and easy to understand.

The book value of an asset can be reduced to Zero.

A fair evaluation of an asset each year on the balance sheet.

Second, among the types of depreciation methods is the diminishing value method which is also known as the Written down value method, Reducing instalment method and Fixed percentage on diminishing balance.

According to the diminishing value method, it is charged on reducing balance & at a fixed rate. In this case, the written down value is spread between the useful life of the asset.

The percentage, at which the shrink happens, remains fixed, however, the amount of depreciation diminishing year after year.

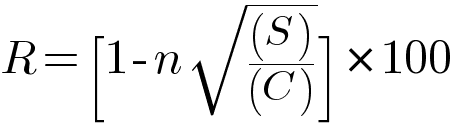

According to the Diminishing Value Method,

R = Rate of Depreciation in %

n = Useful life of the asset in years

S = Residual/Scrap value of the asset

c = Cost of asset

Example – Diminishing Value Method

Asset cost = 1,000,000

Rate of reduction = 20% (DVM)

1st year = 20/100*1,000,000

=>2,00,000

2nd year = 20/100*(1,000,000-2,00,000)

=>1,60,000

Advantages of Diminishing Value Method are;

More practical and easy to apply.

The decreasing charge for depreciation cancels out increasing charges for repairs.

This method is applicable for income tax purposes.

Short Quiz for Self Evaluation

Loading

Your quiz has been submitted

Want to re-attempt? - Simply “refresh” this page.

Please check out more content on our site :)

Subscribed? - Check your mailbox

Thank You!

Server Side Error

We faced problems while connecting to the server or receiving data from the server. Please wait for a few seconds and try again.

If the problem persists, then check your internet connectivity. If all other sites open fine, then please contact the administrator of this website with the following information.

TextStatus: undefined HTTP Error: undefined

Processing you request

Error

Some error has occured.

Revision & Highlights Short Video

Highly Recommended!!

Do not miss our 1-minute revision video. This will help you quickly revise and memorize the topic forever. Try it :)

All expenses incurred before a company is formed i.e. cost incurred before the start of business operations is termed as preliminary expenses. They are a common example of fictitious assets and are written off every year from the profits earned by the business.

Examples of such expenses suffered before the incorporation of business are;

Legal cost (Govt. & Court related fees)

Professional fees (Lawyers, Chartered Accountants, etc.)

Stamp duty

Printing fees

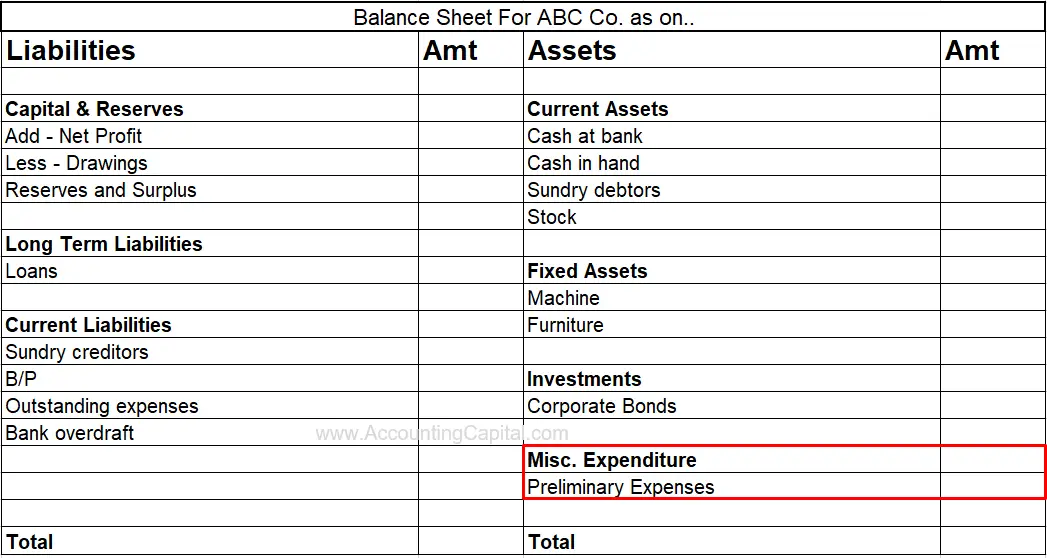

Shown in Financial Statements

Also known as pre-operative expenses, preliminary expenses are shown on the asset side of a balance sheet.

The portion which is written off from the gross profit in the current year is shown on the income statement and the remaining balance is placed in the balance sheet. They are preferably written off within the same year (depending on amount & local accounting standards).

Accounting & Journal Entry for Preliminary Expenses

Stage – I – At the time of payment (Opening Entry)

Suppose company-A incurs a total of 100,000 as expenses before the start of business operations, the below entry will be used to show this.

Preliminary Expenses A/C

1,00,000

Debit the increase in expenses

To Bank

1,00,000

Credit the decrease in assets

(Paid via bank)

Stage – II – Preliminary Expenses Written Off (Indirect Expense)

Then company-A decides to write off the total amount of 100k in 5 years therefore only 1/5th (20,000) will be charged in this year’s income statement and remaining (80,000) will be shown in the balance sheet under the head Miscellaneous Expenditure.

Preliminary Exp. Written Off A/C

20,000

To Preliminary Expenses A/C

20,000

Stage III – Charging to Income Statement (Closing Entry)

Company-A then posts the related expense in the current period’s Profit and Loss Account.

The same entry is repeated for the next 4 years to fully amortize the charge in forthcoming accounting periods.

Profit and Loss A/C

20,000

To Preliminary Expenses A/C

20,000

They are not be confused with pre-commencement costs which are incurred immediately before the commencement of business, however, in this case, the business incorporation is already complete. Pre-commencement expenses are directly charged to the current period’s income statement. Example – Employee recruitment expenses, etc.

Short Quiz for Self-Evaluation

Loading

Your quiz has been submitted

Want to re-attempt? - Simply “refresh” this page.

We have more F&A topics & quizzes :)

Subscribed? - Check your mailbox

Thank You!

Server Side Error

We faced problems while connecting to the server or receiving data from the server. Please wait for a few seconds and try again.

If the problem persists, then check your internet connectivity. If all other sites open fine, then please contact the administrator of this website with the following information.

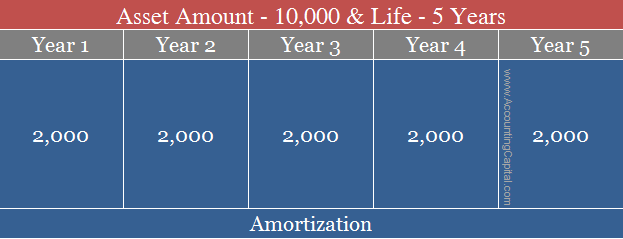

Reduction in the value of an intangible asset by prorating its cost over a period of time (generally in multiple accounting periods) is called Amortization. Point worth remembering is that it can only be done for intangible assets such as copyrights, patents, trademarks, goodwill, etc. It is used for writing-off intangible assets whereas depreciation is used for tangible assets.

If related to obligations, it can also mean payment of any debt in regular instalments over a period of time. Home and other loans often talk about such amortization schedules.

If an intangible asset has an unlimited life then a yearly impairment test is done, which may result in a reduction of its book value.

Suppose a company Unreal Pvt Ltd. develops new software, gets copyright for 10,000, and it is expected to last for 5 years.

Now, if the company shows the entire 10,000 as an expense, it will not show the true and fair picture for that accounting period and the profits for that year will show deflated numbers. Hence, every year the company shall record 2,000 for 5 years to write off the copyright’s entire cost,2,000 X 5 Years

This will be seen as amortization of the copyright with the straight-line method. Writing off the entire copyright’s amount in 5 years over 5 equal instalments.

Accounting & Journal Entry for Amortization

Assuming that no contra account was prepared and the reduction was done directly from the intangible asset, the journal entry would be as follows;

Amortization Expense A/C

Debit

To Intangible Asset A/C

Credit

Only to the extent related to the current financial year, the remaining amount is shown in the balance sheet as an asset.

Short Quiz for Self-Evaluation

Loading

Your quiz has been submitted

Want to re-attempt? - Simply “refresh” this page.

Please check out more content on our site :)

Subscribed? - Check your mailbox

Thank You!

Server Side Error

We faced problems while connecting to the server or receiving data from the server. Please wait for a few seconds and try again.

If the problem persists, then check your internet connectivity. If all other sites open fine, then please contact the administrator of this website with the following information.

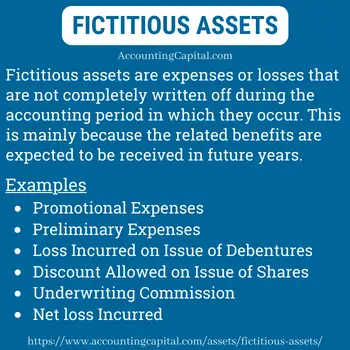

The best way to understand this is to memorize the meaning of the word “fictitious” which means “not true” or “fake”. Fictitious assets are expenses or losses which are not written off completely during the accounting period of their occurrence.

They are not assets at all, however, they are shown as assets in the financial statements only for the time being.

A straightforward example is that of a significant promotional expense. Suppose a small company decides to spend a large sum of 10 Million on marketing a new product and the benefit of such an expense is to last for 5 years.

In year 1, (1/5th) of the total money spent i.e. 2 Million will be shown in the income statement whereas the remaining (4/5th) 8 Million will be shown in the balance sheet as a fictitious asset (under the head Miscellaneous Expenditure).

Important Points

They are written off against the firm’s earnings in more than one accounting period. Basically, they are amortized over a period of time.

They are recorded as assets in financial statements only to be written off in the future.

It is important to note that such assets do not exist physically or have any resale value.

The portion of the expense that is kept for the future is a fictitious asset, while that which is written off in the current period is not.

Reasons why some expenses are not expensed off entirely in the same year

Benefit in the future period – If a business determines that the benefit of an expense or loss will be derived in a future accounting period, then splitting the cost accordingly is both logical and advisable.

Incorrect financial numbers – A firm may not be able to justify its financial statements if they show the entire expense or loss in a single year. It may end up showing an unreasonably large net loss and this may affect the firm’s valuation of goodwill.

In Simple Terms – Fictitious assets are expenses/losses that are not completely written off during the accounting period in which they occur. There is no value in them, but they are still listed as assets in financial statements (temporarily). Why? – because the related benefits of these assets are expected to be received in the future; therefore, showing them as an expense today would do an injustice to the company’s financials.

Examples

Promotional Expenses of a Business

The marketing expenditures of businesses are viewed as investments that are expected to produce long-term returns in future years. The value of these assets is periodically reduced through the process of amortization over a number of years.

Preliminary Expenses

The term “preliminary expenses” refers to all costs incurred before the formation of a business. Examples of such expenses incurred before the incorporation of a business are legal costs, professional fees, stamp duty, printing fees,

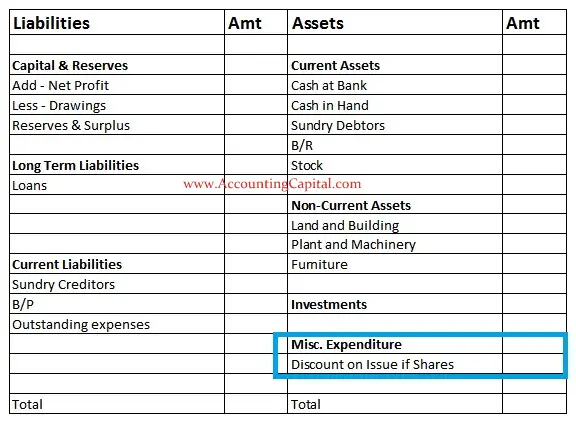

Discount Allowed on the Issue of Shares

An issue of shares at a discount occurs when a company issues its shares for a lower price than its face value. For example, if the face value of a share is 25 and the company issues it at 20, then 5 (25 – 20) is the discount provided by the company on the issue per share.

Now, if the company issues 90,000 such shares at a discount to different investors it would lead to a total loss of 90,000 x 5 = 450,000. Such a loss is treated as a miscellaneous expenditure (fictitious asset).

Loss Incurred on Issue of Debentures

The premium payable on redemption of debentures issued at par or at a discount is a capital loss. For example, if a debenture is issued at a par value of 20, however, the redemption is at a premium i.e. 22 then the loss incurred per debenture is 2 (22 – 20).

Now, if the company issues 80,000 such debenture the total loss incurred at the time of redemption shall be 80,000 x 2 = 160,000. This loss should be appropriately reduced over time.

Underwriting Commission

The underwriting commission is the compensation an underwriter receives from investors for placing a new issue. It is advisable to write off such a fee over time.

Net Loss Incurred by a Company

In some cases, the debit balance of a profit and loss account is also treated as a fictitious asset.

They are shown in the balance sheet on the asset side under the head “Miscellaneous Expenditure”. (To the extent not written off or adjusted)

The amount not written off in the current accounting period is shown on the balance sheet

The above example is provided to demonstrate an expense which may not be treated as an expenditure in the current accounting period, hence it will be recorded as a fictitious asset on the balance sheet.

Why are they shown on the balance sheet?

The organisation will receive returns from these expenses over time, much like it does from other assets. This is the concept behind treating such miscellaneous expenditures as assets.

Depreciation is not possible since they are not tangible, therefore they are amortized as time goes on.

Another way to ask this question is “Are intangible assets such as patents, copyrights, trademarks, etc. also fictitious assets?”.

In short, the answer is No, goodwill is not a fictitious asset and the same is true for other intangible assets.

Acquisitions involve two companies, one purchasing and one being acquired. Goodwill = Purchase price of the targeted/acquired company – (Fair market value of the total assets of the acquired company – Fair market value of the total liabilities of the acquired company)

Reason – An important characteristic of a fictitious asset is that it does not have a realizable value which means it can not be sold in the market to fetch money. However, it is not true for goodwill, patents, and copyrights, since they all have a monetary value and can be sold in the open market.

In addition to this, there is another frequently asked question: Are fictitious assets current assets?

The answer is that all intangible assets are not fictitious assets, however, all fictitious assets are definitely intangible in nature. In spite of this, it is important to note that they are not closely related.

We faced problems while connecting to the server or receiving data from the server. Please wait for a few seconds and try again.

If the problem persists, then check your internet connectivity. If all other sites open fine, then please contact the administrator of this website with the following information.

Fictitious Assets are to be Transferred to Which Account?

This is an accounting FAQ based on the concept of partnership accounting. They are to be transferred to the Partner’s Capital A/c.

As established in the article above that they are considered losses that are not transferred to the realisation account therefore they are transferred to Partner’s Capital account. This is because they are not real assets but are only shown in the financial statements for the time being.

Whenever possible, they are written off against the earnings of the firm. The transfer entry of fictitious assets, if any, is noted as follows:

Such treatment is based on the expectation that it will be beneficial to the business in the long run. This expectation may or may not go as planned and as time progresses, further modifications may be needed.

None of the accounting ratios is affected by these assets because of their false nature. They imitate assets except that they have no intrinsic value, they have no scrap value, and the ultimate goal is to write them off completely with the passing of time.

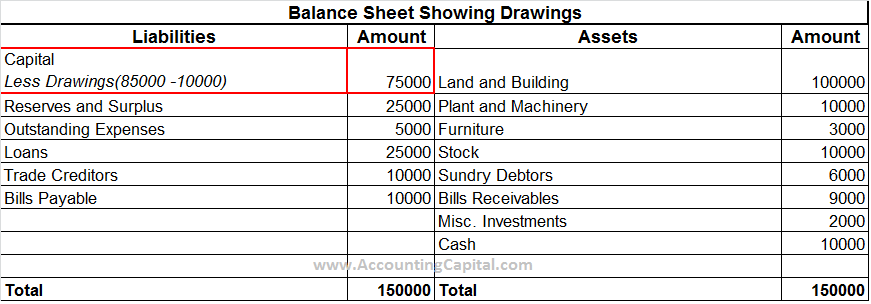

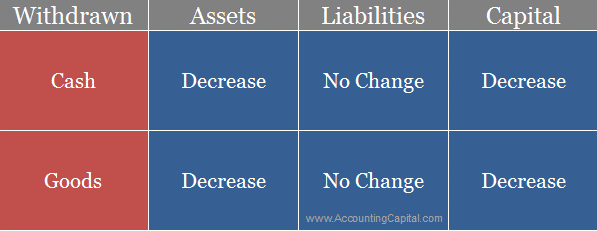

In accounting, assets such as Cash or Goods which are withdrawn from a business by the owner(s) for their personal use are termed as drawings. It is also called a withdrawal account. It reduces the total capital invested by the proprietor(s).

In the case of goods withdrawn by owners for personal use, purchases are reduced and ultimately the owner’s capital is adjusted. The adjustment is done at cost price.

For small firms withdrawals are ordinarily seen in the form of cash or business assets, however, if a business is incorporated they are often observed in the form of dividends or scrip dividends. It is a natural personal account out of the three types of personal accounts.

Journal Entry for Drawings of Goods or Cash

In case of cash withdrawn for personal use from in-hand-cash or the official bank account.

Drawings A/C

Debit

Debit the increase in drawings

To Cash (or) Bank A/C

Credit

Credit the decrease in assets

In case of goods withdrawn for personal use from the business.

Drawings A/C

Debit

Debit the increase in drawings

To Stock A/C

Credit

Credit the decrease in assets

*Purchases account can also be used instead of stock account as the firm’s stock/purchases are being reduced.

It is a temporary account which is cleared during the accounting process at the end of each accounting year & is not shown as a business expense.

A debit balance in drawing account is closed by transferring it to the capital account. It does not directly affect the profit and loss account in any way.

A leather manufacturer withdrew cash worth 5,000 from an official bank account for personal use. Post an appropriate journal entry for this scenario and also show journal entry for adjustment in the capital account.

Journal entry for cash withdrawn for personal use

Drawings A/C

5,000

To Bank A/C

5,000

(Bank balance reduced by 5,000)

Adjustment entry to show the decrease in capital

Capital A/C

5,000

To Drawings A/C

5,000

(Owner’s capital reduced by 5,000)

Type of Account and Where is it Shown in the Financial Statements

It is a Personal A/C and is adjusted from the capital. It is shown in the balance sheet on the liability side as a reduction in capital.

The accounting equation changes with every transaction that happens in a business. Similarly with withdrawals for personal use the accounting equation changes as follows;

Change in the Accounting Equation from Withdrawals for Personal Use

Short Quiz for Self-Evaluation

Loading

Your quiz has been submitted

Want to re-attempt? - “Refresh” this page.

Check out more content on our site :)

Subscribed? - Check your mailbox

Thank You!

Server Side Error

We faced problems while connecting to the server or receiving data from the server. Please wait for a few seconds and try again.

If the problem persists, then check your internet connectivity. If all other sites open fine, then please contact the administrator of this website with the following information.

Financial statements act as a report card for a business. The three major financial statements are prepared as a summary of figures and facts showing the financial condition of a business.

They are not only used to show how a business uses its funds committed by the shareholders and the lenders, but also to see where the business stands in terms of its financial position.

Profit & Loss Account or Income Statement

Balance Sheet or Statement of Financial Position

Cash Flow Statement or Statement Accounting for Variations in Cash

Profit & Loss Account or Income Statement

After the preparation of a trading account, a profit & loss account is prepared to determine the net profit earned or net loss incurred due to the operations of a business. It is an important final account of a business which shows the summarized view of revenues and expenses for a particular accounting period.

In the horizontal form of a P&L account, Gross profit or Gross loss, whatever is determined from the trading account, is transferred accordingly. The debit side will have all expenses and the credit side – all receipts, both arising out of day-to-day activities.

The difference between the two sides of this account is either net profit or net loss, which is then transferred to the capital account.

(Sample Format of a P&L Account)

Dr.

Cr.

Particulars

Amt

Particulars

Amt

To Trading A/C (Gross Loss)

By Trading A/C (Gross Profit)

To Rent

By Commission Earned

To Depreciation

By Bad Debts Recovered

To Bad Debts

By Interest Earned

To Printing & Stationery

By Dividends on Share

To Salaries

By Example Income 1^

To Legal Cost

To Example Expense 1^

By Capital A/C (Net Loss)*

To Capital A/C (Net Profit)*

*Either of the two will appear. ^Any head can be used instead of the example.

Balance Sheet or a Statement of Financial Position

After the preparation of trading and P&L account, a balance sheet is to be prepared. It is a statement that shows a detailed listing of assets, liabilities, and capital demonstrating the financial condition of a company on a given date.

It is not only required to be prepared according to the companies act but also needed to ascertain the financial position of a business.

The liabilities and capital are shown on the left-hand side, whereas the assets are shown on the right-hand side. According to the accounting equation Assets = Capital + Liabilities, the total of the Left-hand side should always be equal to the right-hand side in a balance sheet.

(Sample Format of a Balance Sheet)

Liabilities

Amt

Assets

Amt

Capital

Land & Building

Reserves & Surplus

Plant & Machinery

Outstanding Expenses

Furniture

Loans

Stock

Trade Creditors

Sundry Debtors

Bills Payable

B/R

Misc. Investments

Cash

Total

Total

Cash Flow Statement or Statement Accounting for Variations in Cash

A Cash Flow Statement is a financial statement which is mandatory to be prepared according to the law along with the other two financial statements.

Cash flow statement shows the movement of cash and cash equivalents, it is an in-depth inflow and outflow for a given period of time. The statement shows the net cash flow from operating, investment and financing activities.

A cash flow statement depicts the sources and uses of a company’s cash and equivalents, which is very important information for stakeholders.

(Sample Format of a Cash Flow Statement)

Cash Flow Statement Indirect Method

Amt

Cash flows from operating activities

Net profit before taxation

Adjustments for,

Depreciation

Investment income

Interest expense

Foreign Exchange Loss

Operating profit before working capital changes

Working capital changes:

Add Decrease/Less Increase in Sundry Debtors

Add Decrease/Less Increase in Inventories

Less Decrease/Add Increase in Sundry Creditors

Cash flow from operations

Interest paid

Income taxes paid

Cash flow from extraordinary items

1. Net cash from operating activities

Cash flows from investing activities

Purchase of fixed asset

Proceeds from sale of equipment

Investment income

Dividends Received

2. Net cash spent in investing activities

Cash flows from financing activities

Proceeds from issue of share capital

Proceeds from long-term borrowings

Payment of long-term borrowings

Interest & dividends paid

3. Net cash used in financing activities

Net increase in cash and cash equivalents 1+2+3

Add Cash and cash equivalents at beginning of the period

Cash and cash equivalents at end of the period

Short Quiz for Self-Evaluation

Loading

Your quiz has been submitted

Want to re-attempt? - “Refresh” this page.

Check out more content on our site :)

Subscribed? - Check your mailbox

Thank You!

Server Side Error

We faced problems while connecting to the server or receiving data from the server. Please wait for a few seconds and try again.

If the problem persists, then check your internet connectivity. If all other sites open fine, then please contact the administrator of this website with the following information.

Also known as working assets, it is part of the total capital which is currently employed in a company’s day-to-day operations. Cash or liquid assets vital to run a company’s daily operations are collectively known as Working Capital. It is computed as the difference between current assets and current liabilities.

Evaluation is done to find out if a business has enough current assets to cover all its short-term liabilities. Monitoring helps with efficient management of a company’s operations and maintenance of its short-term financial health.

The volume and composition of working capital vary among different sectors, size, and types of organizations. For example – a manufacturing unit typically sells on credit basis and hence generates plentiful short-term receivables.

On the other hand, a business which runs solely on cash (example – jewellery) may have very few receivables. Another example may be that of a business which only accepts custom orders (example – made to order clothing) may not have a lot of inventory pile-up.

In the case of inadequacy of working assets, current assets are less than current liabilities, which means the company has to pay more money than it will receive in short-term.

Current Assets < Current Liabilities

A poor working capital condition is the first indication of financial problems for a business and shows that it is struggling to keep up with its daily operations.

Excess Working Capital

In cases where current assets are considerably higher as compared to current liabilities, it is said to be an excess of WC.

Current Assets > Current Liabilities

Surplus WC may indicate inefficiency in the way the business operations as it symbolises that current assets are sitting idle and need to be put to better use.

Example

Calculate working assets for the business, with the help of the below extract from a balance sheet.

Liabilities

Amt

Assets

Amt

..

Current Liabilities

Current Assets

Sundry creditors

75,000

Bank

1,00,000

Bills payable

25,000

Cash

50,000

Bank overdraft

75,000

Debtors

1,50,000

..

Current Assets = 1,00,000 + 50,000 + 1,50,000

Current Liabilities = 75,000 + 25,000 + 75,000

Applying the formula = Current Assets – Current Liabilities

= 3,00,000 – 1,75,000

= 1,25,000

Short Quiz for Self-Evaluation

Loading

Your quiz has been submitted

Want to re-attempt? - “Refresh” this page.

Check out more content on our site :)

Subscribed? - Check your mailbox

Thank You!

Server Side Error

We faced problems while connecting to the server or receiving data from the server. Please wait for a few seconds and try again.

If the problem persists, then check your internet connectivity. If all other sites open fine, then please contact the administrator of this website with the following information.

A suspense account is an account temporarily used in general ledger to carry doubtful amounts which can either be a payment or a receipt. Despite considerable efforts, if the reason(s) causing these questionable amounts are not found, the difference in the trial balance is temporarily transferred to a suspense account till it is properly analyzed and classified.

The difference amount is temporarily recorded in a suspense a/c and should be cleared at some point as it possesses a control risk. It is used to mitigate risk which is addressed and when the errors are rectified.

It is used only because a proper account for a particular transaction couldn’t be determined at the time when the transaction was recorded. When the right account is determined, the amount shall be moved from the suspense account to its proper account.

Cash received from Unreal Pvt Ltd. for 5,000 is wrongly posted to Unreal Pvt Ltd’s. account as 50,000, It is however correctly recorded in the cash account.

Cash A/C

50,000

To Unreal Pvt Ltd A/C

50,000

Faulty Journal Entry

Considering the fact that the proper account couldn’t be determined at the time of correction, the journal entry for rectification will be

Unreal Pvt Ltd A/C

45,000

To Suspense A/C

45,000

Rectification entry

What happens in case a suspense account is not closed?

In case a suspense a/c is not closed at the end of an accounting period, the balance in suspense account is shown on the asset side of a balance sheet if it is a “Debit balance”. In case of a “Credit balance”, it is shown on the liability side of a balance sheet.

Short Quiz for Self-Evaluation

Loading

Your quiz has been submitted

Want to re-attempt? - “Refresh” this page.

Check out more content on our site :)

Subscribed? - Check your mailbox

Thank You!

Server Side Error

We faced problems while connecting to the server or receiving data from the server. Please wait for a few seconds and try again.

If the problem persists, then check your internet connectivity. If all other sites open fine, then please contact the administrator of this website with the following information.